I applied for my first credit card in Sri Lanka back in 2014. The bank officer smiled, handed me a brochure with “exclusive rewards” printed in gold foil, and never once mentioned the renewal fee would triple after year one. I learned the hard way that finding the best credit cards in Sri Lanka is not about the glossy brochure. It is about reading the fee schedule, understanding the cashback math, and knowing which bank actually delivers on its promises.

Sri Lanka now has over 2 million active credit cards in circulation, according to Central Bank of Sri Lanka data. Banks are competing harder than ever, rolling out contactless payments, app-based controls, and cashback programs that sound impressive until you read the fine print. The problem is that most articles comparing the best credit cards in Sri Lanka are either outdated, missing half the banks, or written by someone who has never stood in a Sri Lankan bank queue trying to dispute a charge.

I spent the past month going through the latest fee schedules, reward structures, and card benefits from 12 major banks in Sri Lanka. I compared annual fees in LKR, interest rates, Sri Lanka credit card cashback percentages, lounge access, and insurance coverage.

This guide gives you the honest breakdown so you can pick the right card for your spending habits and budget.

In this guide, you will find:

- A ranked comparison of the best credit cards across 12 Sri Lankan banks

- Real annual fees, interest rates, and cashback percentages verified from official bank sources

- Which card is best for everyday spending, fuel, travel, dining, and online shopping

- A comparison table so you can see everything side by side

- Honest assessments of limitations and hidden charges you should know about

Key Takeaways

- DFCC Bank offers the best overall credit card value in Sri Lanka for 2026. Their guaranteed 1% cashback on every single transaction, with no minimum spend requirement and no category restrictions, is the highest flat-rate cashback in the country. The DFCC Visa Infinite card adds airport lounge access and comprehensive travel insurance for frequent travelers. High-income earners can access the DFCC Pinnacle World Mastercard with up to 3% total cashback on fuel, utilities, dining, travel, and overseas spending, while freelancers earning through platforms like Fiverr and Upwork get a dedicated World Mastercard with 2% cashback on foreign currency transactions.

- Commercial Bank has the lowest convenience fees in the industry at 5.50% to 11.5%, making it the smart pick if you frequently use easy payment plans or carry a balance. Their Platinum card also includes travel insurance up to USD 60,000.

- Sampath Bank’s dual-card system is unique. You get both a Visa and an American Express card, giving you the widest acceptance (Visa) plus premium Amex rewards. Their 15% monthly cashback on supermarkets, transport apps, and utilities is strong, but requires a minimum LKR 50,000 monthly spend.

- NTB American Express cards are the only Amex option in Sri Lanka, offering global recognition and premium benefits like Membership Rewards points that do not expire. If you travel internationally often, this is worth considering.

- For state sector employees, Bank of Ceylon offers the cheapest entry with no joining fee and the first year’s annual fee waived. If you work in government and want a basic, low-cost card, BOC is the practical choice.

How Did We Compare and Rank the Best Credit Cards in Sri Lanka?

This credit card comparison Sri Lanka guide evaluates each card across seven weighted factors. Before jumping into the list, here is how I evaluated each card. I did not rank them based on advertising spend or which bank offered the flashiest promotions. I looked at seven factors that actually matter when you use a credit card in Sri Lanka every day:

- Cashback and rewards value (how much you actually earn back on real spending)

- Annual fees (the real cost of holding the card, including renewal)

- Interest rates (what you pay if you carry a balance)

- Acceptance and coverage (does it work everywhere you need it?)

- Additional benefits (lounge access, insurance, easy payment plans)

- Digital experience (mobile app quality, notifications, online controls)

- Customer service (dispute resolution, card replacement speed, support quality)

I weighted cashback and annual fees the heaviest because those two factors determine whether a card actually saves you money or quietly costs you more than you realize.

1. DFCC Bank Credit Cards (Best Overall for Cashback and Value)

DFCC Bank has quietly built the strongest credit card offering in Sri Lanka, and most people do not even know about it. While bigger banks spend millions on advertising, DFCC focused on one thing that actually matters: giving you real money back on every purchase.

Why DFCC Ranks First

The headline feature is simple, as listed on the DFCC Bank credit cards page: guaranteed 1% cashback on every transaction. No categories to track. No minimum spend thresholds. No rotating bonus categories that change every quarter.

Every rupee you spend on a DFCC credit card earns 1% cashback, credited directly to your account. For overseas transactions, that rate increases to 1.5% cashback. That partially offsets the foreign currency markup most banks charge.

To put this in perspective, if you spend LKR 100,000 per month on your DFCC card (groceries, fuel, dining, utilities, online shopping), you earn LKR 1,000 back every single month. That is LKR 12,000 per year in pure cashback. Most other banks either cap their cashback, restrict it to specific merchant categories, or require you to accumulate points that lose value when you try to redeem them.

But DFCC does not stop at the standard 1% cashback. They have built a tiered credit card ecosystem that rewards higher earners, salary account holders, and even freelancers with significantly better cashback rates and premium benefits that go well beyond what the basic card tiers offer.

DFCC Card Tiers

DFCC Pinnacle World Mastercard (Best for High-Income Earners)

The DFCC Pinnacle World Mastercard is the most rewarding credit card in Sri Lanka for high earners, and it comes with zero joining and annual fees for life. That is not a first-year waiver. It is lifetime free.

The cashback structure on this card is the most generous in the country: 1% cashback on every spend, plus an additional 2% cashback on fuel, utility bill payments, dining, travel, and overseas transactions. That means you earn a total of 3% cashback on five of the most common spending categories for Sri Lankan professionals. If you spend LKR 80,000 per month across fuel, utilities, dining, and travel, that is LKR 2,400 back every month, or LKR 28,800 per year, on top of the 1% you earn on everything else.

The easy payment plans are structured for larger purchases: 0% interest for 6 months on transactions between LKR 50,000 and LKR 200,000, and 0% interest for 12 months on transactions between LKR 200,000 and LKR 2,000,000. These plans exclude fuel, cash advances, casino, and gambling transactions.

Pinnacle cardholders also receive four complimentary airport lounge visits per year via Priority Pass, complimentary travel insurance, global concierge services, and access to Mastercard Priceless benefits. You also get a dedicated relationship manager and access to a 24/7 Pinnacle call centre on 011-2350011.

To qualify for Pinnacle, you need to meet one of the following criteria: a minimum monthly net salary of LKR 500,000 remitted to a DFCC account, a total deposit portfolio of LKR 10,000,000, or a monthly investment commitment of LKR 150,000 for at least five years. Immediate family members can also qualify under the Pinnacle Family scheme if the primary account holder maintains the deposit criteria.

DFCC Prestige Credit Card (Best for Mid-Range Salary Earners)

If your salary falls between LKR 150,000 and LKR 499,999 per month, the DFCC Prestige Credit Card hits the sweet spot between value and accessibility. Like the Pinnacle card, the Prestige card comes with waived joining and annual fees, so you pay nothing to hold this card.

The cashback structure mirrors Pinnacle’s core benefit: 1% cashback on every spend, plus an additional 2% cashback on fuel and utility bill payments made directly to the service provider. That totals 3% cashback on fuel and utilities, which are unavoidable monthly expenses for most Sri Lankan households. If your combined monthly fuel and utility spending is LKR 30,000, you earn LKR 900 back every month, or LKR 10,800 per year, just from paying bills you would pay anyway.

The Prestige card includes 0% interest for 6-month instalment plans on transactions above LKR 25,000 (excluding fuel, cash advances, casinos, and gambling), complimentary travel insurance when you purchase return air tickets using the card, and one free airport lounge visit annually via Lounge Key.

You qualify for Prestige by meeting any one of these criteria: a monthly net salary between LKR 150,000 and LKR 499,999 remitted to a DFCC account, a deposit portfolio exceeding LKR 2,500,000, a personal loan exceeding LKR 3,500,000, or a housing loan exceeding LKR 5,000,000.

DFCC World Mastercard for Freelancers (Best for Platform-Based Workers)

This is a card that most credit card comparison guides completely ignore, but it matters for a growing segment of Sri Lanka’s workforce. The DFCC World Mastercard Freelancer Credit Card is specifically designed for people earning income through platforms like Fiverr, Upwork, and Freelancer.com.

If you are a freelancer, you know the problem: most banks in Sri Lanka do not know how to evaluate platform-based income, and getting approved for a credit card with variable monthly earnings is difficult. DFCC solved this by creating a dedicated freelancer banking proposition that recognizes platform earnings as legitimate income.

The 2% cashback on foreign currency transactions is particularly valuable for freelancers because most of their income and spending (software subscriptions, international tools, hosting, advertising) involves foreign currency. If you spend USD 200 per month on international services and tools, the 2% cashback returns roughly USD 4 per month, or nearly USD 50 per year.

To qualify, you need to provide proof of consistent earnings in excess of LKR 100,000 per month and at least six months of work history on an eligible platform. The mandatory 5% recovery via standing instruction means DFCC automatically deducts 5% of your outstanding balance from your linked account, which helps freelancers with variable income avoid missed payments.

Freelancers also qualify for DFCC’s premium banking tiers based on income: Pinnacle for those earning LKR 500,000 or more per month, Prestige for LKR 150,000 or more, Salary Partner for LKR 50,000 or more, and Salary Plus for LKR 25,000 or more.

The DFCC Lanka IOC Card for Fuel Savings

If you drive regularly, the DFCC Lanka IOC Co-branded Mastercard deserves special attention. It offers 5% cashback at all Lanka IOC fuel stations on top of the standard 1% cashback on everything else. With fuel prices in Sri Lanka hovering around LKR 370 to 400 per liter for petrol, a monthly fuel bill of LKR 15,000 saves you LKR 750 every month, or LKR 9,000 per year, just from filling up your tank at IOC stations.

Key Features Across All DFCC Cards

- Interest-free period: 21 to 51 days (if you pay the full balance by the due date)

- Cash advance limit: 50% of credit limit

- Minimum payment: 5% of balance or LKR 250, whichever is higher

- Supplementary cards: Up to 6 for family members

- Digital banking: DFCC One mobile app with real-time notifications, card controls, and e-statements

- Contactless payments: NFC-enabled for tap-and-go transactions

- Security: 24/7 transaction monitoring with SMS alerts

- 0% easy payment plans: 6 and 12 month installment options on selected purchases over LKR 25,000, including insurance payments

- Online credit card application: You can apply for any DFCC credit card online without visiting a branch, and the DFCC sales team will contact you to complete the process

Who Should Get a DFCC Card

DFCC is the best choice for anyone who wants straightforward, guaranteed cashback without playing the category games that other banks require. If you spend broadly across groceries, dining, fuel, online shopping, and utilities, no other bank in Sri Lanka gives you a better flat-rate return on your total spending. The Visa Infinite tier is particularly strong for frequent travelers who want lounge access and travel insurance bundled into one card.

For high-income professionals earning LKR 500,000 or more, the Pinnacle World Mastercard delivers the highest total cashback in the country at up to 3% on key categories, with a lifetime-free annual fee and four airport lounge visits per year. Mid-range salary earners between LKR 150,000 and LKR 499,999 get nearly identical cashback benefits through the Prestige card, also with waived fees. And freelancers working on international platforms finally have a bank that understands their income structure and offers a dedicated credit card with 2% cashback on the foreign currency transactions that dominate their spending.

Honest Limitations

DFCC Bank has a smaller branch network than Commercial Bank, Sampath, or HNB, with over 133 branches island-wide. If you prefer walking into a branch for card issues, you might find fewer locations in rural areas compared to the largest banks. However, DFCC has significantly reduced this friction by allowing you to apply for credit cards entirely online through their website, and their DFCC One mobile app handles most card management tasks without needing a branch visit. Their credit card acceptance at smaller merchants is also slightly less established compared to Visa cards from bigger banks, though this gap has narrowed significantly with the growth of digital payments.

I switched to DFCC from a bigger bank two years ago specifically for the flat cashback. The math is simple: I spend around LKR 150,000 monthly on the card, and I get LKR 1,500 back every month without thinking about it. No points to track, no categories to remember. It just works.

2. Commercial Bank Credit Cards (Best for Low Fees and Easy Payment Plans)

Commercial Bank is the largest private bank in Sri Lanka by assets, and their credit card operation reflects that scale. They process more transactions than almost any other bank on the island, which gives them the leverage to offer some of the most competitive fee structures in the industry.

Why Commercial Bank Ranks Second

The standout advantage is their convenience fee of just 5.50% to 11.5%, which is the lowest in the Sri Lankan banking industry. If you regularly convert large purchases into easy payment installments, this lower fee saves you real money compared to banks charging 15% to 18% for the same service. Their interest rates sit at 24% to 26% per annum, which is competitive for Sri Lanka.

Card Tiers and Requirements

Commercial Bank offers Gold/Silver and Platinum tiers:

- Gold/Silver Credit Card: Minimum income of LKR 50,000 per month. Available in Visa, Mastercard, UnionPay, and LankaPay/JCB options.

- Platinum Credit Card: Minimum gross salary of LKR 125,000 per month. Minimum credit limit of LKR 250,000.

- Anagi Credit Card: Designed specifically for women, with tailored benefits.

Key Benefits

- Travel insurance: Free overseas cover up to USD 60,000 for 60 days when you purchase your return airfare on the card. This is one of the most generous complimentary travel insurance packages in Sri Lanka.

- Concierge services: 24/7 access for travel bookings, restaurant reservations, business assistance, sports and entertainment tickets.

- Multiple card networks: Choose between Visa, Mastercard, UnionPay, or LankaPay/JCB depending on where you shop most.

- Interest-free period: Up to 51 days if you pay the full balance.

- Auto-settlement: Set up automatic payment from your savings or current account so you never miss a due date.

- Digital banking: ComBank Digital app and ePassbook for real-time tracking.

Who Should Get a Commercial Bank Card

If you frequently use easy payment plans to split large purchases into installments, Commercial Bank’s low convenience fees make it the most cost-effective option. Their travel insurance is also strong for the Platinum tier. This is a solid all-rounder from Sri Lanka’s most established private bank.

Honest Limitations

Commercial Bank’s reward and cashback programs are less generous than DFCC’s flat 1% cashback. Their points system requires more effort to track and redeem, and the per-point value is lower than what you get from DFCC’s direct cashback. If maximizing rewards is your priority, DFCC wins. If minimizing fees on installment purchases is your priority, Commercial Bank wins.

3. Sampath Bank Credit Cards (Best Dual-Card System with High Category Cashback)

Sampath Bank runs the most unique credit card setup in Sri Lanka: when you apply, you receive both a Visa card and an American Express card. This dual-card system gives you the best of both worlds. Use the Visa for everyday purchases at any merchant (Visa is accepted almost everywhere in Sri Lanka), and switch to the Amex for premium rewards at Amex-accepting merchants.

Why Sampath Ranks Third

The dual-card approach is genuinely clever. But the real draw is their 15% monthly cashback on supermarkets, transport apps (PickMe, Uber), and utility payments. That is an aggressive cashback rate, though it comes with conditions: you need to spend a minimum of LKR 50,000 per month to activate the cashback, and the 15% applies only to those specific categories.

Sampath also publishes their fee schedule transparently. Their credit card charges document (available as a PDF on their website) lists every fee, from annual charges to late payment penalties, in clear detail. That transparency is worth noting because not every bank makes this information easy to find.

Key Features

- Dual cards: Visa + American Express issued together

- 15% cashback: On supermarkets, transport apps, and utilities (minimum LKR 50,000 monthly spend)

- 0% installment plans: Available across a wide network of partner merchants

- Comprehensive promotions: Sampath runs some of the most active credit card promotion programs, with discounts at restaurants, hotels, and retailers across Sri Lanka

- Mobile banking: Sampath Vishwa app for card management

Who Should Get a Sampath Card

Sampath is ideal if your monthly spending is concentrated on groceries, utilities, and transport. The 15% cashback on those categories is hard to beat, though you need to hit the LKR 50,000 minimum spend. The dual-card system is a genuine advantage for people who shop both locally (Visa) and at premium/international merchants (Amex).

Honest Limitations

The minimum spend requirement for cashback activation means low spenders will not benefit. If your total credit card spending is under LKR 50,000 per month, DFCC’s no-minimum 1% cashback will serve you better. Also, not all merchants in Sri Lanka accept American Express, so your Amex card will sit unused at many smaller shops and restaurants outside Colombo.

4. Nations Trust Bank American Express (Best Premium and Travel Card)

Nations Trust Bank (NTB) is the sole issuer of American Express cards in Sri Lanka. If you want an Amex card without the dual-system approach of Sampath, NTB is your only option. And for frequent international travelers, the Amex brand carries genuine weight.

Card Tiers

- Blue American Express Card: Entry-level Amex with standard rewards

- Platinum American Express Card: Premium tier with enhanced dining, wellness, travel, and entertainment benefits

Why NTB Amex Ranks Fourth

The key advantage is Membership Rewards points that do not expire as long as your account remains active. Most other Sri Lankan bank reward programs expire points after 2 to 3 years, which means you lose value if you do not redeem regularly. With NTB Amex, your points accumulate indefinitely.

The Platinum card comes with access to the American Express global network of benefits: airport lounge access through Priority Pass or Amex-affiliated lounges, travel insurance, purchase protection, and exclusive dining and entertainment offers. These benefits are genuinely useful for people who travel internationally several times per year.

Key Features

- Membership Rewards: Points that never expire (while account is active)

- Global recognition: American Express is accepted at premium merchants worldwide

- Dining and entertainment: Exclusive restaurant and hotel offers in Sri Lanka and internationally

- Travel benefits: Airport lounge access, travel insurance, baggage protection on Platinum tier

- Installment plans: 0% payment plans at partner merchants

- Online security: Amex SafeKey for secure online transactions

Who Should Get an NTB Amex Card

This card is best for frequent international travelers and people who value premium lifestyle benefits. If you fly out of Sri Lanka more than 3 to 4 times per year, the lounge access and travel insurance alone can justify the annual fee. The non-expiring rewards points are a genuine differentiator. If you travel internationally, check which visa-free countries for Sri Lankan passport holders you can visit with your credit card travel insurance covering the trip.

Honest Limitations

American Express acceptance in Sri Lanka is limited compared to Visa and Mastercard. You will find Amex accepted at major hotels, airlines, large retailers, and upscale restaurants, but your neighborhood grocery store, local pharmacy, and most small merchants will not accept it. You need a Visa or Mastercard as your primary daily card and the Amex as a secondary for premium purchases and travel.

5. HSBC Credit Cards (Best International Bank Option)

HSBC is the largest international bank operating in Sri Lanka, and their credit card products reflect a global banking perspective. If you already bank with HSBC or handle significant international transactions, their cards offer integration advantages that local banks cannot match.

Card Tiers

Why HSBC Ranks Fifth

The HSBC Visa Platinum Cashback card offers a structured cashback of up to LKR 12,000 per year, broken down as 10% cashback (capped at LKR 1,000 per month) on mobile, fuel, and supermarket expenses, plus an unlimited 0.1% on all other purchases. With a minimum monthly spend of LKR 25,000, this delivers consistent value.

The HSBC Live+ card pushes category cashback further with 10% on dining, shopping, and entertainment. If your spending is concentrated in those categories, the returns are strong.

Key Features

- Global banking integration: Seamless connection to HSBC accounts in other countries

- Forex advantages: Competitive foreign currency conversion rates for international spending

- Premier relationship: High-net-worth clients get the Premier Mastercard with dedicated relationship manager, global lounge access, and preferential rates

- Digital banking: HSBC Sri Lanka mobile app with real-time spend tracking and card controls

Who Should Get an HSBC Card

HSBC cards are best for people who bank internationally, handle foreign currency transactions regularly, or qualify for the Premier tier through high deposit balances. If you are a non-resident looking to open a bank account as a non-resident, HSBC’s global network makes the process smoother than local banks. The structured cashback on the Platinum card is competitive, but the real value comes from the global banking ecosystem.

Honest Limitations

HSBC has a very limited branch network in Sri Lanka, with branches concentrated primarily in Colombo. If you live outside the Western Province, resolving card issues in person is inconvenient. Their customer service, while professional, can feel impersonal compared to local banks that know their customers by name.

6. HNB Credit Cards (Best Branch Network for Support)

Hatton National Bank (HNB) operates one of the largest branch networks in Sri Lanka, with over 250 branches and 800+ ATMs across all nine provinces. If physical accessibility and in-person customer service matter to you, HNB has an advantage that no international bank or smaller local bank can match.

Key Features

- Massive branch network: Over 250 branches across Sri Lanka, including rural areas where other banks have limited presence

- 0% installment plans: 3, 6, and 12 month easy payment options with no handling fees on eligible purchases

- Visa and Mastercard options: Choose your preferred card network

- HNB SOLO app: Digital banking with card controls, spend tracking, and instant notifications

- Merchant partnerships: Strong network of partner merchants offering discounts and deals, particularly in Colombo and major cities

- Supplementary cards: Available for family members with shared credit limit

Card Tiers

HNB offers Classic, Gold, Platinum, and Signature tiers with increasing benefits and credit limits. The Platinum and Signature cards include travel insurance and airport lounge access.

Who Should Get an HNB Card

HNB is the practical choice if you live outside Colombo or need reliable in-person banking support. Their branch network means you can walk into an HNB branch in almost any town in Sri Lanka to resolve card issues, make payments, or get assistance. The 0% easy payment plans are competitive, and the merchant discount network is extensive.

Honest Limitations

HNB’s cashback and rewards programs are not as generous as DFCC’s flat 1% or Sampath’s category-specific 15%. The card is more about convenience and accessibility than maximizing rewards. If you are a rewards optimizer, look elsewhere. If you value support and accessibility, HNB delivers.

7. Bank of Ceylon Credit Cards (Best for State Sector Employees)

Bank of Ceylon (BOC) is Sri Lanka’s oldest bank, established in 1939, and was the first bank to introduce credit cards to Sri Lanka in 1989. That history gives BOC a unique position in the market, particularly for government and state sector employees who enjoy preferential terms.

Why BOC Ranks Here

The standout benefit for state sector employees: no joining fee and the first year’s annual fee waived. For government workers on modest salaries, this removes the financial barrier to getting a credit card. BOC also offers salary-linked credit limits, making approval easier for state sector workers with steady but lower incomes. If you are considering a career in banking, see our guide on the qualifications to become a bank manager in Sri Lanka.

Key Features

- State sector benefits: No joining fee, first year free for government employees

- Pioneer status: Sri Lanka’s longest-running credit card operation

- BOC SmartPay app: Mobile payment and card management

- Wide branch network: BOC has one of the largest branch networks in Sri Lanka as a state bank

- Low entry barrier: Accessible credit limits for lower-income applicants

- Fuel surcharge: 1% surcharge applicable for fuel, liquor, and cigarettes (factor this into your cost calculations)

Card Tiers

BOC offers Classic, Gold, and Platinum tiers. The credit limits and benefits scale with income and banking relationship.

Who Should Get a BOC Card

BOC is the right choice for state sector employees who want a no-cost entry into credit cards, and for anyone who prefers banking with the stability and reach of a state-owned institution. If you already have your salary account with BOC, the integration and approval process is straightforward.

Honest Limitations

BOC’s digital banking experience lags behind private banks like DFCC, Commercial Bank, and Sampath. The mobile app and online portal are functional but not as polished. Reward programs are basic compared to the competition. The 1% fuel surcharge also reduces your effective savings if you use the card for petrol.

8. Seylan Bank Credit Cards (Best for Dining and Lifestyle Discounts)

Seylan Bank has positioned its credit card offering around lifestyle discounts and extended installment plans. If you eat out frequently or make large purchases that you want to spread across longer periods, Seylan’s terms are attractive.

Key Features

- Up to 30% off dining: Seylan credit cards offer up to 30% off total bills at partner restaurants (20% off on bills above LKR 5,000)

- Extended installment plans: 0% installment options for up to 36 months, which is longer than most other banks in Sri Lanka

- Visa card options: Multiple tiers from Classic through to Signature Premier

- Seylan Bank app: Digital card management with spend tracking

- Merchant partnerships: Growing network of partner retailers and service providers

Card Tiers

Seylan offers Classic, Gold, Platinum, and Visa Signature Premier tiers. The Signature Premier is their top-tier card with the highest credit limits and most comprehensive benefits.

Who Should Get a Seylan Card

If you are a frequent diner who spends regularly at restaurants, Seylan’s 30% dining discounts can save you significant money over a year. Pair a Seylan card with our guide to the best dinner buffets in Colombo to maximize your savings. The 36-month installment plans are also the longest in the market, useful for large purchases like electronics, furniture, or home appliances.

Honest Limitations

Seylan’s cashback and general rewards are not as strong as DFCC or Sampath. The value is concentrated in dining discounts and installment flexibility. If you do not eat out often or rarely use installment plans, you will not extract enough value from this card to justify it over a flat-cashback option.

9. Standard Chartered Credit Cards (Best for Air Miles and SriLankan Airlines Flyers)

Standard Chartered’s partnership with SriLankan Airlines makes their credit card the go-to option for frequent flyers on the national carrier. If you accumulate SriLankan Airlines FlySmiLes miles, this card accelerates your earning.

Key Features

- SriLankan Airlines partnership: Earn FlySmiLes miles on every transaction

- Complimentary companion ticket: Platinum cardholders can earn a free companion air ticket upon reaching minimum annual spend thresholds

- Airport lounge access: Available on premium tiers

- Global acceptance: Visa and Mastercard options with worldwide coverage

- Rewards credit card: Dedicated rewards card for non-travel focused spending

Who Should Get a Standard Chartered Card

This card makes sense only if you fly SriLankan Airlines frequently enough to benefit from FlySmiLes mile accumulation and the companion ticket offer. For travelers who fly the national carrier 4+ times per year, the accumulated miles and free companion ticket can deliver several thousand rupees in value.

Honest Limitations

If you do not fly SriLankan Airlines regularly, the card’s primary advantage disappears. Standard Chartered’s branch network in Sri Lanka is limited, and their general cashback and rewards are not competitive with DFCC or Sampath for everyday spending.

10. People’s Bank Credit Cards (Best Budget Option for Low-Income Earners)

People’s Bank, as a state-owned institution, focuses on financial inclusion. Their credit card products are designed with lower income thresholds and simpler fee structures than private banks.

Key Features

- Low income requirements: Some of the most accessible credit card entry points in Sri Lanka

- State bank stability: Backed by the government of Sri Lanka

- Wide branch network: Extensive presence across all provinces, including rural areas

- Basic rewards: Simple points-based reward program

- Salary integration: Easy approval for People’s Bank salary account holders

Who Should Get a People’s Bank Card

This is a practical entry-level option if your income does not meet the minimums set by private banks. People’s Bank makes credit accessible to a broader segment of Sri Lankan workers, particularly those in the state sector or lower-income brackets.

Honest Limitations

The rewards, cashback, and digital experience are the most basic in this comparison. This is a utility card, not a rewards card. If you qualify for cards at DFCC, Commercial Bank, or Sampath, those banks will deliver more value.

11. Pan Asia Banking Corporation (PABC) Credit Cards

Pan Asia Banking Corporation offers credit cards primarily through Visa, targeting mid-market customers who want a straightforward card without the complexity of tiered reward programs.

Key Features

- Simple fee structure: Transparent pricing without hidden charges

- Visa acceptance: Standard Visa network coverage across Sri Lanka and internationally

- Personal banking integration: Works best for existing PABC customers

- Easy payment plans: Standard installment options at partner merchants

Who Should Get a PABC Card

PABC cards are best for existing PABC banking customers who want the convenience of a credit card from their primary bank. The card is functional and reliable but does not offer standout rewards or benefits compared to larger banks.

Honest Limitations

PABC’s branch network, rewards program, and digital banking experience are less developed than the larger banks in this list. The card works, but it does not compete on rewards or benefits.

12. Union Bank Credit Cards

Union Bank rounds out this comparison as a smaller player in the Sri Lankan credit card market. Their cards offer basic functionality with straightforward terms.

Key Features

- Visa cards: Standard Visa acceptance

- Competitive interest rates: Union Bank’s rates are generally in line with industry averages

- Digital banking: Basic online and mobile banking capabilities

- Easy payment plans: Installment options at selected partner merchants

Who Should Get a Union Bank Card

Similar to PABC, Union Bank cards are most relevant for existing Union Bank customers. If you already bank with Union Bank and want a credit card from your primary institution for convenience, it works. Otherwise, the larger banks offer more value.

Honest Limitations

Limited branch network, basic rewards, and a smaller merchant partnership network compared to the top banks in this list.

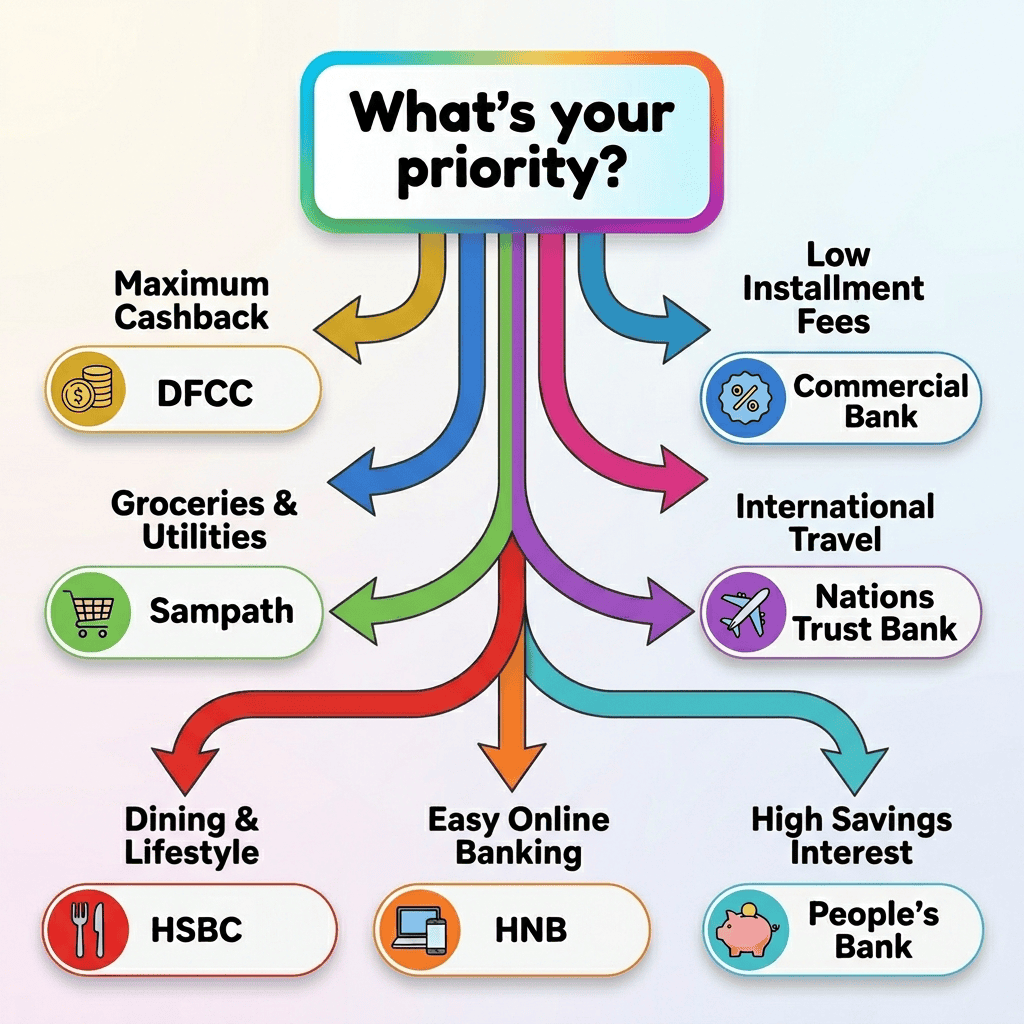

Which Bank Has the Best Credit Card in Sri Lanka for 2026?

The answer depends on your spending pattern, but DFCC Bank wins for overall value with guaranteed 1% flat cashback on every purchase, Commercial Bank wins for lowest installment fees, and Sampath Bank wins for category-specific cashback on groceries and utilities. Here is the full credit card comparison Sri Lanka breakdown:

Complete Comparison Table

How Do You Choose the Best Credit Card in Sri Lanka for Your Needs?

Picking the best credit card Sri Lanka 2026 depends entirely on how you spend. The right card matches your spending pattern to the bank that rewards it most. Here is a simple decision framework:

If You Want Maximum Cashback on Everything

Pick DFCC Bank. The flat 1% cashback with no minimum spend, no category restrictions, and no points-to-redeem hassle is the simplest and most effective way to earn rewards in Sri Lanka. Add the Lanka IOC card for 5% fuel cashback if you drive regularly. If your salary exceeds LKR 150,000, the Prestige or Pinnacle cards push your cashback to 3% on fuel and utilities, with waived annual fees for life.

If You Are a Freelancer Earning Through International Platforms

Pick the DFCC World Mastercard Freelancer card. It is the only credit card in Sri Lanka specifically designed for platform-based workers on Fiverr, Upwork, and Freelancer.com. The 2% cashback on foreign currency transactions directly rewards the way freelancers spend, and DFCC’s freelancer banking proposition makes approval straightforward with documented platform earnings. You can apply online by selecting “Freelancer” as your employment type.

If You Use Easy Payment Plans Frequently

Pick Commercial Bank. Their convenience fees of 5.50% to 11.5% are the lowest in Sri Lanka. If you regularly split large purchases (electronics, furniture, appliances) into monthly installments, Commercial Bank saves you the most on those transaction fees. Easy payment plans are especially useful when buying and selling in Sri Lanka, where large purchases on electronics and furniture benefit from split payments.

If Your Spending Is Concentrated on Groceries and Utilities

Pick Sampath Bank. The 15% cashback on supermarkets, transport apps, and utilities is hard to beat in those specific categories. But make sure your monthly card spending exceeds LKR 50,000 to qualify.

If You Travel Internationally Often

Pick NTB American Express (for global Amex benefits and non-expiring points) or Standard Chartered (for SriLankan Airlines FlySmiLes miles and companion tickets). If you qualify for the DFCC Pinnacle World Mastercard, its four complimentary Priority Pass lounge visits and travel insurance make it a strong contender in this category as well.

If You Work in the State Sector

Pick Bank of Ceylon. No joining fee and free first-year annual fee makes this the most affordable entry into credit cards for government employees.

If You Need Reliable Branch Support Outside Colombo

Pick HNB. Their 250+ branches across all nine provinces means you can get in-person help in almost any town in Sri Lanka.

If You Eat Out Frequently

Pick Seylan Bank. Up to 30% off at partner restaurants adds up fast if you dine out multiple times per week.

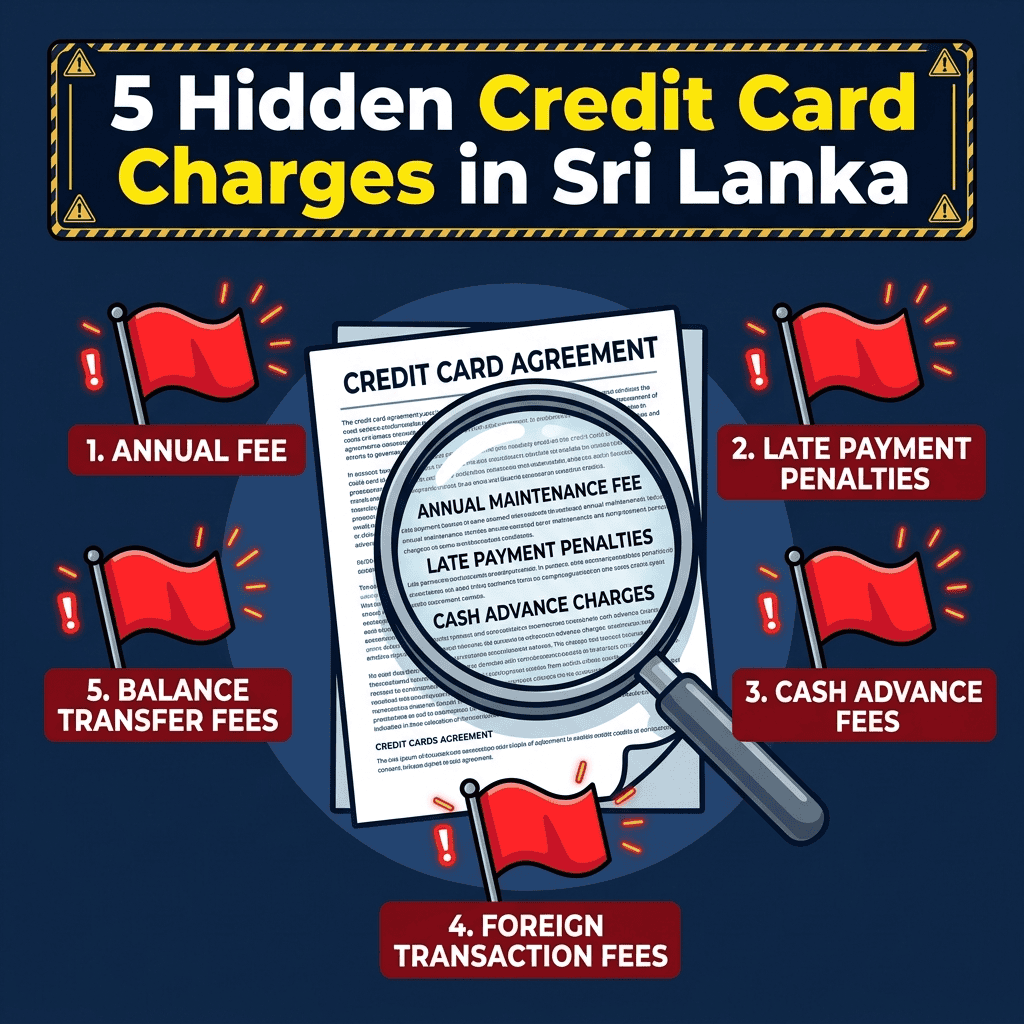

What Are the Hidden Charges on Sri Lankan Credit Cards?

Even the best credit cards in Sri Lanka come with annual renewal fees, cash advance fees, late payment penalties, foreign currency markups, and fuel surcharges that are not obvious when you sign up. Before you apply, here are charges that catch most first-time cardholders off guard:

Annual Fee Traps

Many banks offer free first-year annual fees to attract new customers. The renewal fee in year two can be LKR 2,000 to LKR 8,500 depending on the card tier. Always ask about the renewal fee before applying, and check whether the bank waives it if you meet a minimum annual spend threshold. Notable exceptions include the DFCC Pinnacle World Mastercard and DFCC Prestige Credit Card, both of which come with lifetime-free annual fees as part of their salary banking propositions.

Cash Advance Fees

Using your credit card at an ATM to withdraw cash is one of the most expensive mistakes you can make. Most banks charge 2% to 5% of the withdrawal as a fee (minimum LKR 250 to 500), and interest starts accruing immediately with no interest-free period. Avoid cash advances entirely.

Late Payment Charges

Missing your minimum payment deadline triggers a late fee (typically LKR 500 to 1,500) and can also increase your interest rate on future purchases. Set up auto-debit from your bank account to avoid this.

Foreign Currency Markup

When you use your credit card overseas or for international online purchases (in USD, GBP, EUR), banks add a currency conversion markup of 2.5% to 3.5% on top of the exchange rate. DFCC’s 1.5% cashback on overseas transactions partially offsets this, which is why it ranks first for international spending too. The DFCC Freelancer card’s 2% cashback on foreign currency transactions offers an even stronger offset for platform-based workers making regular international payments.

Fuel Surcharge

Some banks (including BOC) add a 1% surcharge on fuel purchases. This directly reduces any cashback you earn. Check your bank’s fuel surcharge policy before using your credit card at the pump.

Balance Transfer Limitations

Unlike credit card markets in the US or UK, balance transfer offers in Sri Lanka are rare and limited. Most Sri Lankan banks do not offer promotional 0% balance transfer rates. If you are carrying a balance on a high-interest card, your best option is to negotiate directly with your bank for a lower rate or consolidate through a personal loan rather than expecting a balance transfer deal.

Over-Limit Fees

Exceeding your credit limit triggers a fee of LKR 500 to 1,000 at most banks. Monitor your spending through your bank’s mobile app to avoid hitting the ceiling.

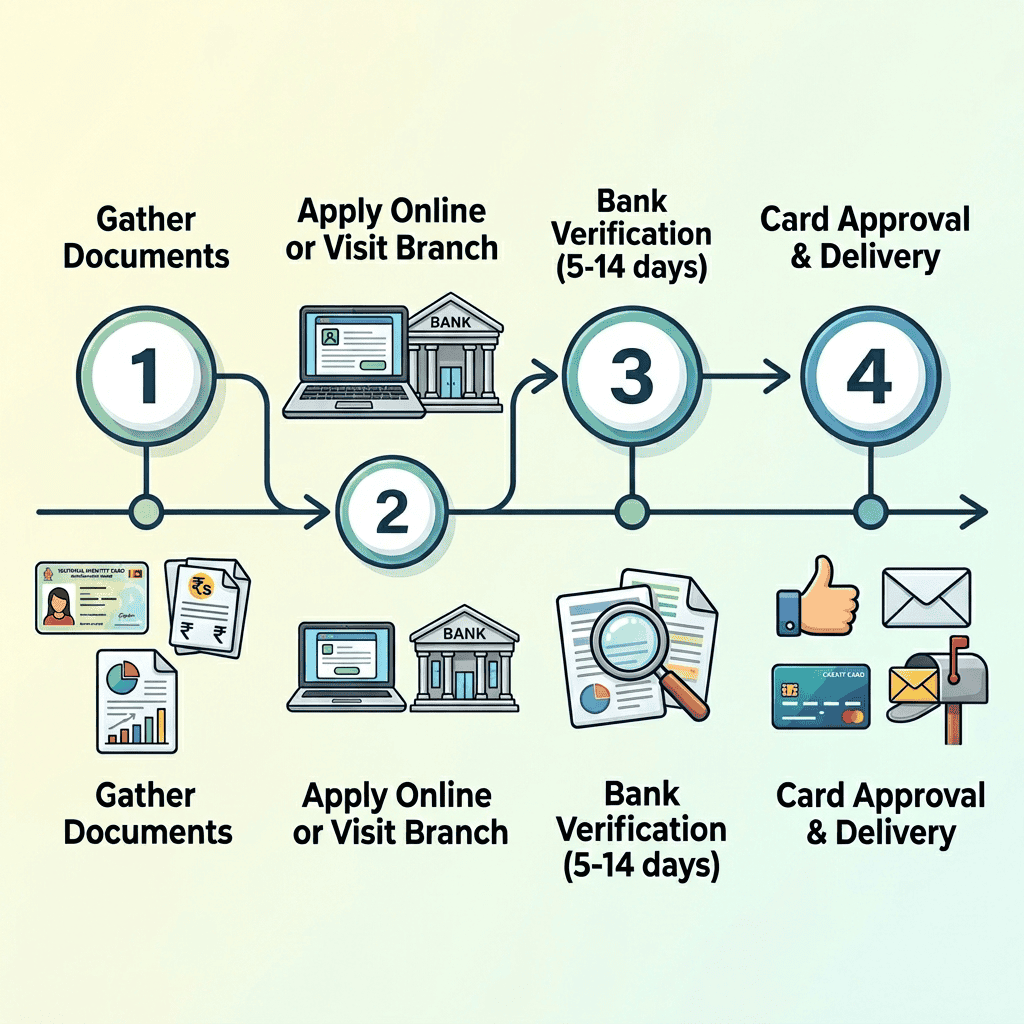

How Do You Apply for a Credit Card in Sri Lanka?

Once you have identified the best credit cards in Sri Lanka for your needs, applying requires your NIC, proof of income (3 months salary slips), recent bank statements, and proof of address, with most banks now accepting online applications alongside branch visits. The application process is similar across all banks:

Documents Required

- NIC (National Identity Card) or valid passport

- Proof of income: Latest 3 months’ salary slips, or income tax returns for self-employed applicants. Freelancers applying for the DFCC Freelancer card need proof of platform earnings and at least six months of work history on an eligible platform.

- Bank statements: Last 3 to 6 months from your current bank

- Proof of address: Utility bill (electricity, water, phone) dated within the last 3 months, or a Gramasevaka certificate

- Employment confirmation letter: From your employer confirming position and salary

Application Methods

- Online: Most banks now accept online applications through their websites. DFCC Bank’s online credit card application portal lets you apply for any of their cards, including the Pinnacle, Prestige, Freelancer, and standard tiers, without visiting a branch. The DFCC sales team contacts you after submission to complete the process. Commercial Bank, Sampath, HSBC, and others also offer online applications.

- Branch visit: Walk into any branch with your documents

- Phone: Some banks process applications initiated through their call centers

Approval Timeline

Expect 5 to 14 working days from application to receiving your card. Banks with simpler verification processes (like DFCC and Commercial Bank) tend to be faster. BOC and People’s Bank may take longer due to additional state-sector verification steps.

Frequently Asked Questions

What is the best credit card in Sri Lanka for everyday spending?

DFCC Bank’s credit cards offer the best value for everyday spending in 2026, with a guaranteed 1% cashback on every transaction regardless of merchant category or spending amount. No other bank in Sri Lanka offers a flat-rate cashback this generous without minimum spend requirements. If you qualify for the DFCC Prestige or Pinnacle tiers, your cashback increases to 3% on fuel, utilities, dining, travel, and overseas spending.

Which Sri Lankan bank has the lowest credit card interest rate?

Commercial Bank offers some of the most competitive interest rates at 24% to 26% per annum, along with the lowest convenience fees in the industry at 5.50% to 11.5%. If you occasionally carry a balance or use easy payment plans, Commercial Bank minimizes your interest costs.

Can I get a credit card in Sri Lanka with a low salary?

Yes. Bank of Ceylon and People’s Bank offer credit cards with lower income requirements than private banks. BOC also waives the joining fee and first-year annual fee for state sector employees. DFCC and Commercial Bank have entry-level cards starting at LKR 50,000 to 100,000 minimum monthly income.

Which credit card has the best cashback for fuel in Sri Lanka?

The DFCC Lanka IOC Co-branded Mastercard offers 5% cashback at all Lanka IOC fuel stations, which is the highest fuel-specific cashback rate among Sri Lankan credit cards. This is in addition to the standard 1% cashback on all other purchases. The DFCC Prestige and Pinnacle cards also offer 3% total cashback on fuel (1% base plus 2% additional on fuel), which applies at any fuel station rather than just Lanka IOC.

Is there a credit card for freelancers in Sri Lanka?

Yes. DFCC Bank offers the World Mastercard Freelancer Credit Card, specifically designed for platform-based workers earning through Fiverr, Upwork, Freelancer.com, and similar platforms. It offers 1% cashback on LKR transactions, 2% cashback on foreign currency transactions, and 0% easy payment plans for up to 6 months. You need to show consistent earnings above LKR 100,000 per month and at least six months of platform work history to qualify.

Is American Express accepted everywhere in Sri Lanka?

No. American Express acceptance is limited compared to Visa and Mastercard. Amex is accepted at major hotels, airlines, large retailers, and upscale restaurants, but most smaller merchants, neighborhood shops, and local businesses do not accept it. Always carry a Visa or Mastercard as your primary card.

How many credit cards should I have in Sri Lanka?

For most Sri Lankans, one or two credit cards is enough. A primary card for everyday spending (like DFCC for flat cashback) and optionally a second card for specific benefits (like Sampath for grocery cashback or Standard Chartered for airline miles) gives you good coverage without overcomplicating your finances.

Do Sri Lankan credit card reward points expire?

Most banks expire reward points after 2 to 3 years. The notable exception is NTB American Express Membership Rewards, which do not expire as long as your card account remains active. DFCC avoids this issue entirely by paying direct cashback instead of points.

What happens if I miss a credit card payment in Sri Lanka?

Missing a payment triggers a late fee (LKR 500 to 1,500) and interest charges on your outstanding balance (24% to 36% per annum depending on the bank). It also leaves a negative mark on your CRIB (Credit Information Bureau) report.

Your CRIB score is Sri Lanka’s equivalent of a credit score. It affects your ability to get future loans, credit cards, and even some job applications. Two or more missed payments can damage your CRIB rating for years.

Set up auto-debit from your bank account to avoid missed payments. If you are struggling to pay, contact your bank immediately to discuss restructuring options before your account goes into default.

Final Verdict

The best credit card in Sri Lanka for 2026 depends on your spending habits, but if I had to pick one card for the average Sri Lankan consumer, it would be DFCC Bank. The guaranteed 1% cashback on every transaction, with no minimum spend and no category games, delivers the most consistent value across all spending patterns. Add the Lanka IOC card for fuel savings, and you have a combination that is hard to beat. High earners who qualify for the Pinnacle World Mastercard get up to 3% cashback on key categories with a lifetime-free card, four airport lounge visits, and travel insurance. Freelancers earning through international platforms get a dedicated card with 2% foreign currency cashback that no other bank in Sri Lanka offers.

For specific use cases, Commercial Bank wins on installment fees, Sampath wins on grocery cashback, NTB Amex wins for international travelers, and BOC wins for state sector employees on a budget.

The worst thing you can do when choosing the best credit cards in Sri Lanka is to pick one based on the sign-up bonus or first-year free offer without checking the renewal fees, cashback conditions, and hidden charges. Read the fee schedule. Do the math on your actual monthly spending. Then choose the card that puts the most money back in your pocket. You can apply for a DFCC credit card online without visiting a branch if you have decided on their offering.

If you are looking to make money online in Sri Lanka or register a business, a good credit card with proper cashback management becomes even more valuable for managing business expenses.

For more financial guidance, explore our Sri Lankan finance guides covering everything from health insurance to loan apps.

Last verified: April 2026. Credit card fees, interest rates, and promotions change frequently. Always confirm current terms directly with the issuing bank before applying. Advice.lk updates this guide regularly as banks revise their offerings.

Disclosure: This guide is independently written. Advice.lk does not accept payments from banks to influence rankings. Some links may be affiliate links. Both referral and non-referral links are provided where applicable, giving you the choice.