Kumari earned Rs. 85,000 a month at a garment factory in Katunayake. For three years, her salary landed in a regular savings account at the nearest bank branch. No cashback. No salary advance facility. No credit card tie-in. No preferential loan rates. When her colleague showed her a payslip with a free credit card, 2x salary overdraft, and 1% cashback on every swipe, Kumari thought it was a scam. It was not. It was a salary savings account from a competing bank, and her colleague had been using it since day one.

That gap between a regular savings account and the best salary savings account in Sri Lanka is costing thousands of workers real money every month. I checked, and nearly every major bank in Sri Lanka now offers a salary-linked account with benefits you will never get from a standard savings product. Free credit cards with waived annual fees. Salary advances before payday. Overdraft facilities at 2x to 3x your monthly salary. Preferential interest rates on personal loans and housing loans. Free digital banking and SMS alerts.

I compared the best salary savings account in Sri Lanka options across 12 banks, checking their salary thresholds, credit card perks, loan benefits, overdraft limits, and digital banking features. Whether you earn Rs. 25,000 or Rs. 500,000 a month, this guide helps you pick the account that gives you the most value for your salary deposit. DFCC Bank offers three distinct salary tiers for mid-career and executive-level earners, but the right choice depends on your salary level and what matters most to you.

Want to grow your savings further? Check our guide to the best women savings account in Sri Lanka if you are eligible for additional women-specific benefits on top of your salary account perks.

Key Takeaways

- DFCC Bank offers a comprehensive salary banking proposition with three tiers (Salary Partner, Prestige, and Pinnacle) for eligible mid-career and executive-level earners.

- Commercial Bank Achiever is the strongest option for mid-range earners who want salary advances and a well-established digital banking platform with the widest ATM network in the country.

- HNB Salary Smart stands out for its aggressive overdraft facility, offering up to 3x your monthly salary as an OD limit after qualifying salary credits.

- Most salary accounts require zero balance to open, with the first salary credit expected within 30 days. The real differences are in credit card perks, loan rates, and overdraft limits.

- Every salaried employee in Sri Lanka should switch to a salary savings account if they are still using a regular savings account. The benefits are strictly better, and there is no additional cost.

What Is a Salary Savings Account in Sri Lanka?

A salary savings account is a specialized bank account that Sri Lankan banks offer exclusively to employees who receive their monthly pay through direct deposit. Unlike regular savings accounts, salary accounts bundle free credit cards, cashback rewards, overdraft (OD) facilities, and preferential loan rates at zero extra cost, making them strictly better than standard accounts for every salaried worker.

It gives you everything a regular savings account offers, plus a package of benefits that banks reserve exclusively for salary customers.

Here is what changes when you move from a regular savings account to a salary-linked one:

The logic behind every salary savings account Sri Lanka banks offer is straightforward. Banks want your salary deposit because it is predictable, recurring revenue. In exchange, they give you benefits that cost them very little but save you real money. If you are a salaried worker in Sri Lanka earning Rs. 25,000 or more per month and you are not using a salary savings account, you are leaving free money on the table.

How Did I Pick the Best Salary Savings Account in Sri Lanka?

I assessed each bank’s salary savings account across seven factors:

-

Salary threshold: The minimum monthly salary required to qualify

-

Credit card perks: Free cards, cashback rates, installment plans

-

Overdraft facility: OD limit as a multiple of salary, qualifying period

-

Loan benefits: Preferential rates on personal, housing, and vehicle loans

-

Digital banking: Mobile app quality, online features, SMS alerts

-

ATM access: Free withdrawal network coverage across Sri Lanka

-

Extra perks: Insurance, lifestyle discounts, priority banking, airport lounge access

I also checked whether each account requires a branch visit to open or supports digital onboarding, because not everyone lives within easy reach of a bank branch.

1. DFCC Bank Salary Proposition (Best Overall for Rs. 50,000+)

DFCC Salary Proposition salary savings account Sri Lanka

DFCC Salary Proposition salary savings account Sri Lanka

Bank: DFCC Bank

Best For: Mid-career professionals to corporate executives

Why First: Three distinct salary tiers with benefits that scale as your career grows

DFCC Bank is one of the strongest salary savings account providers in Sri Lanka for 2026 because it does not force everyone into the same product. Instead, DFCC offers three separate salary tiers, each designed for a different income bracket with benefits that scale as your career grows. No other bank in Sri Lanka gives you this level of segmentation.

The three tiers are Salary Partner, Prestige, and Pinnacle.

What makes DFCC stand out further is the digital infrastructure. DFCC offers 10 financial calculators on their website covering home loans, personal loans, fixed deposits, and retirement planning. You can apply for accounts and credit cards online without visiting a branch. And DFCC’s Investment Planner tool helps you map out long-term savings goals, something no other Sri Lankan bank offers as a self-service digital tool.

Let me break down each tier.

DFCC Salary Partner (Mid-Level: Rs. 50,000+)

Minimum Net Salary: Rs. 50,000 per month remitted to a DFCC account

Best For: Mid-career professionals, private sector employees, teachers, nurses

This is where DFCC’s salary proposition gets seriously competitive. Salary Partner is the sweet spot for most Sri Lankan professionals, and the benefits package rivals what some banks offer only to their premium customers.

Credit Card Benefits:

- Free DFCC Credit Card with joining and annual fees waived (minimum salary Rs. 75,000 for credit card qualification)

- 1% cashback on every purchase you make with the card

- 2% cashback on fuel and utility bill payments made directly to service providers

- 0% interest installment plans for 6 months on transactions between Rs. 25,000 and Rs. 1,000,000

That 0% installment facility is a standout. Most banks charge 12-18% interest on installment plans. DFCC gives you six months interest-free on purchases from Rs. 25,000 up to Rs. 1,000,000. Buy a laptop, a washing machine, or furniture, and pay it off over six months without a single rupee in interest. This applies to DFCC credit card transactions across retail partners island-wide.

Overdraft Facility:

- Available after 6 consecutive monthly salary deposits

- OD limit: 2x your net monthly salary, up to Rs. 300,000

- No collateral required

Six months of consistent salary credits, and DFCC gives you an unsecured overdraft at twice your salary. If you earn Rs. 75,000, that is Rs. 150,000 available as an OD. If you earn Rs. 150,000, you get the maximum Rs. 300,000.

Personal Loan Benefits:

- Preferential interest rates (lower than standard personal loan rates)

- Maximum tenure: 7 years

- Approval within 3 working days

Digital Banking:

- Free DFCC ONE mobile app and online banking

- Free SMS alerts, eStatements, utility bill payments with no service charges

- Free ATM withdrawals from any DFCC or LankaPay ATM nationwide

Honest Assessment: DFCC Salary Partner is the account I recommend for most working Sri Lankans earning Rs. 50,000 or more. The 1% cashback on all spending, 2% on fuel, 0% installments, and 2x salary OD after six months make this genuinely hard to beat. The credit card requires Rs. 75,000 minimum salary though, so if you earn Rs. 50,000-74,999, you get the savings account benefits but not the credit card.

DFCC Prestige (Senior Level: Rs. 150,000+)

Minimum Net Salary: Rs. 150,000 to Rs. 499,999 per month

Alternative Qualifications: Deposit portfolio above Rs. 2,500,000, or personal loan above Rs. 3,500,000, or housing loan above Rs. 5,000,000

Best For: Senior managers, department heads, experienced professionals

DFCC Prestige takes everything from Salary Partner and adds premium lifestyle benefits.

Credit Card Benefits (Same cashback, better perks):

- 1% cashback on every spend, 2% on fuel and utility payments

- 0% interest installment plans for 6 months on Rs. 25,000 to Rs. 1,000,000

- Complimentary travel insurance when you purchase return airfare with the card

- One free airport lounge visit annually via Lounge Key

That airport lounge access alone is worth Rs. 5,000-8,000 per visit. If you travel internationally even once a year, this pays for itself.

Loan Benefits:

- Preferential interest rates on personal and housing loans

- Priority processing with faster approval timelines

- Higher loan limits based on Prestige qualification

Account Features:

- Zero-balance savings and current accounts

- No minimum balance maintenance fee on current account

- Account sweeping facility between savings and current accounts

- Free debit card with waived fees

- 24/7 dedicated call centre for priority customer service

- Free ATM withdrawals at DFCC and LankaPay ATMs nationwide

Honest Assessment: If you earn Rs. 150,000 or more, Prestige is an obvious upgrade. The airport lounge access and travel insurance transform the credit card from a spending tool into a travel companion. The preferential loan rates save you real money on housing loans, which is where the biggest savings happen. A 0.5% reduction on a Rs. 10,000,000 housing loan saves you over Rs. 500,000 across a 20-year term.

DFCC Pinnacle (Executive Level)

Best For: Corporate executives, C-suite leaders, high-net-worth professionals

DFCC Pinnacle is the top-tier proposition, targeting high-income executives who need personalized banking.

Key Benefits:

- Exclusive premier banking services with priority across all channels

- Dedicated Relationship Manager assigned to your account

- High-value private banking loans at special rates

- Premium investment solutions tailored to your portfolio

- Seamless digital banking via DFCC ONE and online banking

- Premium lifestyle benefits including dining, travel, and shopping discounts

- Minimum 1% cashback on daily transactions

Honest Assessment: DFCC does not publicly disclose specific salary thresholds or detailed benefit amounts for Pinnacle on their website. This tier is relationship-based, meaning you likely need to be referred through your employer’s corporate banking relationship with DFCC, or have a significant deposit/loan portfolio. If you qualify, the dedicated Relationship Manager alone makes it worthwhile, as you stop waiting in queues and dealing with call centres forever.

Why DFCC Leads the Market

Nalini works as an HR manager earning Rs. 120,000 a month. She opened a DFCC Salary Partner account, got a free credit card within two weeks, and started earning 1% cashback on groceries at Keells and 2% back on every CPC fuel fill. Six months in, she qualified for a Rs. 240,000 overdraft that she used to cover her mother’s hospital bill without touching her savings. When she needed a personal loan for home renovations, DFCC approved it in three days at a preferential rate. She did all of this through the DFCC ONE app without visiting a branch once.

That is the DFCC salary account experience in practice.

Where DFCC falls short: DFCC has only around 140 branches and 200 ATMs across Sri Lanka. Compare that to Commercial Bank’s 900+ ATMs or BOC’s 600+ branches. If you live in a rural area or outside the Western Province, accessing a DFCC branch can be inconvenient. The DFCC ONE app and LankaPay ATM network help, but they do not fully close the gap. Also, DFCC’s credit card requires a minimum Rs. 75,000 salary, which locks out Salary Partner customers earning Rs. 50,000-74,999 from the card benefits. And Pinnacle’s lack of publicly disclosed thresholds makes it hard to plan for.

Ready to check if the DFCC salary account is right for your income level? Use the DFCC financial calculators to estimate your loan eligibility, fixed deposit returns, or retirement savings goal before you apply.

Which Bank Has the Best Salary Account for ATM Access?

Commercial Bank Achiever salary savings account Sri Lanka

Commercial Bank Achiever salary savings account Sri Lanka

Commercial Bank’s Achiever salary account gives you access to the widest private bank ATM network in Sri Lanka, with over 900 ATMs and 269+ branches across all 25 districts, making it the top choice for employees who travel for work or live outside Colombo.

Bank: Commercial Bank of Ceylon

Account Name: Achiever Current Account / Achiever Salary Account

Best For: Employees who need the widest private bank ATM and branch network plus salary advance access

Why Consider: Largest private bank ATM network (900+), salary advance facility, and credit card eligibility from Rs. 40,000 salary

Commercial Bank is Sri Lanka’s largest private commercial bank by assets, and their Achiever account is purpose-built for salary customers.

Salary Threshold and Eligibility

- Minimum salary: Typically Rs. 30,000+ with a corporate salary arrangement between your employer and Commercial Bank

- Credit card minimum income: Rs. 50,000/month (general applicants) or Rs. 40,000/month if your salary is remitted directly to a ComBank account

- Account type: Current account (not savings), which means chequebook access and no withdrawal limits

The lower credit card threshold for salary customers (Rs. 40,000 vs Rs. 50,000) is a notable advantage for workers in the Rs. 40,000-49,999 bracket who cannot qualify for credit cards at most other banks.

Credit Card Benefits

Commercial Bank offers Visa, Mastercard, UnionPay, and LankaPay (JCB) credit cards. Achiever salary account holders get:

- Free joining fee and annual fee for the first year

- 50% cashback up to Rs. 1,000 on the first POS or online transaction after card activation (minimum transaction Rs. 2,000)

- Interest-free installment schemes at partner merchants

- 6 convenient settlement cycles for flexible payment management

- Payment settlement at any of 269+ branches nationwide

The first-year fee waiver is standard across Sri Lankan banks, but the 50% cashback on the first transaction is a decent welcome bonus. After the first year, annual fees apply at standard ComBank rates.

Salary Advance Facility

This is the Achiever account’s headline feature. Commercial Bank offers salary advances for urgent cash needs before payday. The advance is typically a percentage of your monthly salary, credited to your account within hours of request. Exact advance percentages and qualifying periods depend on your salary level and employment history with the bank.

Overdraft Facility

Available after establishing a salary credit history (typically 6 consecutive salary deposits). The OD limit is based on your salary level, generally 1.5x to 2x your net monthly salary. Exact terms are determined during assessment.

Digital Banking: ComBank Digital

- ComBank Digital app (iOS and Android): One of the most polished banking apps among Sri Lankan private banks

- Fund transfers (intra-bank and inter-bank via SLIPS/CEFT)

- Bill payments and utility settlements

- Credit card management and payments

- QR code payments via LANKAQR

- Fixed deposit placement

- Real-time balance and transaction alerts

- 24/7 customer hotline: 011 2353 353

Branch and ATM Network (Commercial Bank’s Killer Feature)

- 269+ branches across all 25 districts

- 900+ ATMs island-wide (largest private bank ATM network)

- International debit card accepted at Visa/Mastercard merchants globally

- Free ATM withdrawals at Commercial Bank machines

If you travel for work between Colombo, Kandy, Galle, Jaffna, and Batticaloa, Commercial Bank’s ATM coverage means you will almost always find a machine nearby. No other private bank matches this footprint.

Loan Benefits

- Preferential personal loan rates for Achiever account holders

- Housing loan priority processing with preferential rates

- Vehicle loan facilities at competitive terms

- Loan applications can be initiated through ComBank Digital

Kasun is a sales executive covering the Eastern and Northern provinces. His Rs. 72,000 salary goes into a Commercial Bank Achiever account because he needs cash access everywhere he travels. In Trincomalee, Batticaloa, and Jaffna, he finds ComBank ATMs at every town centre. When his car needed emergency repairs in Ampara, he used the salary advance to cover Rs. 35,000 without waiting for payday. The ComBank Digital app let him check his account balance and approve the advance from his phone while standing at the mechanic’s shop.

Honest Assessment: Commercial Bank wins on accessibility. The 900+ ATM network and 269+ branches make it the most physically accessible private bank in Sri Lanka. The salary advance facility is genuinely useful, and the lower credit card threshold (Rs. 40,000 for salary customers) opens card access to more workers. The digital app is above average.

The weakness is transparency. Commercial Bank’s salary account benefits are not as clearly tiered or publicly documented as DFCC’s three-tier system. You may need to visit a branch to understand exactly what you qualify for. The credit card cashback (50% on first transaction only) is a one-time welcome bonus, not an ongoing benefit like DFCC’s 1% on every purchase. And the Achiever account is a current account, not a savings account, so your idle balance earns less interest than it would in a savings product. For maximum cashback and OD benefits, DFCC Salary Partner is better. For maximum physical accessibility, Commercial Bank Achiever is the clear winner.

Which Salary Account Offers the Highest Overdraft in Sri Lanka?

HNB Salary Smart offers the highest overdraft multiple among Sri Lankan salary accounts, giving you up to 3x your net monthly salary as an unsecured OD facility after 3-6 consecutive salary deposits. For a Rs. 100,000 salary, that is Rs. 300,000 available on demand, no collateral needed.

Bank: Hatton National Bank

Account Name: HNB Salary Smart

Best For: Employees who want maximum borrowing power against their salary

Minimum Salary: Rs. 35,000 net per month

HNB is Sri Lanka’s fourth-largest private commercial bank by assets, with a well-established corporate banking franchise. HNB Salary Smart is their dedicated salary account product, and its standout feature is the overdraft facility that beats every competitor on the multiple.

Salary Threshold and Eligibility

- Minimum net salary: Rs. 35,000 per month remitted directly to an HNB account

- No minimum balance requirement to maintain the account

- Zero account opening charge for salary customers

- Employer arrangement: Your company needs to have a corporate salary arrangement with HNB, or you can request one through your HR department. HNB actively onboards new corporate clients.

Overdraft Facility (HNB’s Killer Feature)

This is where HNB beats everyone:

For a Rs. 100,000 salary, that is Rs. 300,000 available on demand. Compare that to DFCC’s 2x (Rs. 200,000) or Sampath’s 2x (Rs. 200,000). The difference is Rs. 100,000 in emergency borrowing power, which is significant when you are facing an unplanned hospital bill or urgent home repair.

The qualifying period (3-6 months) depends on your employer’s arrangement with HNB. Companies with long-standing corporate relationships get the 3-month qualifying period; newer arrangements may require 6 months. Once activated, the OD renews automatically as long as your salary continues.

Salary Advance

- Available for mid-month cash needs before payday

- Processed through HNB Mobile or branch request

- Repaid automatically from the next salary credit

The salary advance is separate from the OD facility. You can use both, though the OD is more flexible since it functions like a revolving credit line.

Credit Card Benefits

HNB offers credit cards to Salary Smart customers with waived fees:

- HNB SOLO Debit Card: Free, annual fee waived for salary customers

- HNB Credit Cards: Visa Classic, Gold, and Platinum tiers available

- Joining fee: Waived for salary customers

- Annual fee: First year free; subsequent years waived based on spend thresholds

- Installment plans: Available at HNB partner merchants

- Cash advance: Available at ATMs

HNB’s credit card offering is functional but not market-leading. DFCC Salary Partner gives you 0% installment plans up to 60 months and 1% cashback; HNB’s cashback structure is less transparent and the installment plan terms are not as generous. If credit card perks are your priority, DFCC or Commercial Bank are stronger choices.

Loan Benefits

HNB offers preferential rates for Salary Smart customers on:

- Personal loans: Special interest rates below standard retail rates

- Housing loans: Preferential rates; HNB is a major housing loan provider in Sri Lanka

- Vehicle loans: Reduced rates for salary account holders

- Education loans: Available for salary customers with children in higher education

The exact preferential rate depends on your salary level and employer relationship. HNB does not publish a fixed “salary customer discount” percentage like BOC’s 0.5% concession; instead, you negotiate based on your profile. This can work in your favour if you are a high earner, but means less pricing transparency for mid-range salary earners.

Digital Banking

HNB Mobile Banking App:

- Fund transfers (own accounts, third-party, interbank via CEFT/SLIPS)

- Bill payments and utility payments

- QR payments (LANKAQR compatible)

- Account balance and transaction history

- Credit card payments and management

- Fixed deposit opening

- Biometric login (fingerprint/face ID)

HNB Internet Banking (Web):

- Full banking functionality including bulk transfers

- Statement downloads

- Standing order management

HNB’s mobile app is competent but does not match Sampath Vishwa’s feature depth or ComBank Digital’s polish. It covers all essential banking functions reliably, which is what most users need.

Branch and ATM Network

HNB’s branch network is concentrated in urban and semi-urban areas. It covers all major cities and district capitals but is thinner in deep rural areas compared to BOC (660+) or People’s Bank (700+). For someone working in Colombo, Kandy, Galle, or Kurunegala, HNB access is not an issue. For remote postings, check branch availability in your area first.

Unique Perks

- HNB Priority Banking: Higher-salary customers get access to priority counters and dedicated relationship managers

- Free SMS alerts for all transactions

- Free eStatements (no physical statement charges)

- Corporate partnership benefits: If your employer has a strong relationship with HNB, you may get additional perks like higher OD multiples or faster approval times

Honest Assessment

Nimal, an IT project manager earning Rs. 120,000 at a software company in Colombo, kept his salary at a bank that offered only a 1x OD facility. When his mother needed emergency knee replacement surgery costing Rs. 350,000, his 1x OD of Rs. 120,000 was not enough. He had to take a personal loan at 18% interest for the difference. A colleague at the same company banked with HNB Salary Smart and had a 3x OD of Rs. 360,000, enough to cover the same surgery without touching a personal loan. That OD interest, charged only on the amount used and only for the days used, cost a fraction of what a personal loan would have.

Strengths: Highest OD multiple in the market (3x salary), solid branch network in urban areas, preferential rates across personal/housing/vehicle loans, reliable digital banking, zero account opening charges.

Weaknesses: Credit card perks are not as generous as DFCC or Commercial Bank. Cashback structure lacks transparency. Loan rate discounts are negotiable rather than fixed, which means less predictability. The app is functional but not best-in-class. Branch network is thinner in rural areas compared to BOC or People’s Bank.

Pick HNB if: Your top priority is borrowing power and emergency liquidity. The 3x OD gives you the biggest safety net of any salary account. Skip HNB if: You want the best credit card cashback, the best app experience, or the widest rural branch coverage.

Which Sri Lankan Bank Has the Best Salary Account App?

Sampath Bank Salary salary savings account Sri Lanka

Sampath Bank Salary salary savings account Sri Lanka

Sampath Bank’s Sampath Salary Plus account pairs with the Sampath Vishwa mobile app, widely regarded as the most feature-rich banking app in Sri Lanka. It supports biometric login, QR payments, salary advances, bill payments, loan applications, and even contactless NFC payments through Sampath WePay, all from your phone without visiting a branch.

Bank: Sampath Bank

Account Name: Sampath Salary Plus / Sampath Salary Savings Account

Best For: Tech-savvy employees who want the best mobile banking experience

Minimum Salary: Rs. 30,000 net per month (corporate arrangements may vary)

Sampath Bank is Sri Lanka’s third-largest private commercial bank and has invested heavily in digital banking. The bank has won multiple digital banking awards in the region, and the Sampath Vishwa app is consistently rated as one of the best banking apps in Sri Lanka.

Salary Threshold and Eligibility

- Minimum net salary: Rs. 30,000 per month

- Corporate salary arrangement required (Sampath actively onboards employers)

- Zero balance account opening for salary customers

- Salary must be credited within 30 days of account opening

Credit Card Benefits

Sampath offers a tiered credit card system for salary customers:

- Sampath Visa Classic / Mastercard Standard: For salaries Rs. 30,000+

- Sampath Visa Gold / Mastercard Gold: For salaries Rs. 50,000+

- Sampath Visa Platinum: For higher-income brackets

- Joining fee: Waived for salary customers

- Annual fee: First year free, subsequent years waived based on spending thresholds

- Installment plans: 0% plans available at Sampath partner merchants (electronics, home appliances, education)

- Cashback: Available on select merchant categories

- Sampath Loyalty Points: Earn points on every transaction, redeem for rewards

The credit card offering is solid but middle-of-the-pack. DFCC’s 1% universal cashback and 60-month installment plans are more generous. Sampath’s advantage is the seamless app integration; you manage your entire credit card lifecycle (application, limit increase, payments, dispute resolution) from the Vishwa app without visiting a branch.

Overdraft Facility

- Up to 2x monthly salary after qualifying period

- Qualifying period: 3-6 consecutive salary deposits

- Unsecured (no collateral required)

- Interest charged daily on the amount used

Standard across the industry at 2x. HNB beats this with 3x. But Sampath’s OD is easily managed through the app; you can check your available OD limit, draw down funds, and track interest charges in real-time from your phone.

Salary Advance

- Available through the Sampath Vishwa app (no branch visit needed)

- Processed within minutes during banking hours

- Repaid automatically from the next salary credit

- Available after 3 consecutive salary remittances

The ability to request a salary advance from your phone at 11 PM on a Sunday and have it processed by Monday morning is Sampath’s real convenience play. Most other banks require a branch visit or at minimum a phone call during business hours.

Loan Benefits

Sampath offers preferential rates for salary account holders on:

- Personal loans: Reduced interest rates, faster approval

- Housing loans: Competitive rates with longer tenures

- Vehicle loans/leasing: Special packages for salary customers

- Education loans: Available for higher education financing

- Loan applications via app: You can apply for and track loans entirely through Sampath Vishwa

Digital Banking (Sampath’s Killer Feature)

This is where Sampath genuinely leads the market:

Sampath Vishwa Mobile App:

- Biometric login (fingerprint, face ID)

- Fund transfers (own accounts, third-party, interbank via CEFT/SLIPS)

- QR code payments (LANKAQR certified) at 100,000+ merchant locations

- Bill payments (utilities, insurance, school fees, government payments)

- Loan applications and tracking

- Fixed deposit opening and renewal

- Credit card management (payments, limit increase requests, dispute resolution)

- Salary advance requests

- Account statements and transaction history

- Push notifications for all transactions

- Multi-currency account access

Sampath PayZ (Contactless Payments):

- NFC-based contactless payments from your phone

- Works at any PayWave/PayPass terminal

- No physical card needed

- Transaction limits configurable in the app

Sampath WePay (Digital Wallet):

- Digital wallet for online and in-store payments

- QR code generation for receiving payments

- Peer-to-peer transfers

- Merchant payments without exposing card details

Sampath Internet Banking (Web):

- Full banking functionality for desktop users

- Bulk transfers and corporate banking features

- Tax payments and government service fees

- Statement downloads in multiple formats

The difference between Sampath’s digital suite and most competitors is polish. HNB’s app does the basics. ComBank Digital is feature-rich. But Sampath Vishwa feels like it was designed by people who actually use banking apps daily. The navigation is intuitive, the response times are fast, and the QR payment experience at merchants is the smoothest I have tested.

Branch and ATM Network

Sampath’s physical network is smaller than BOC (660+), People’s Bank (700+), or Commercial Bank (269+). The 12 “super branches” are flagship locations in major cities that offer extended hours and premium service. For most transactions, you will not need a branch at all; the app handles nearly everything.

Unique Perks

- Sampath Star Loyalty Programme: Earn points on debit and credit card transactions, redeem for vouchers, merchandise, and experiences

- Free SMS alerts for all account and card transactions

- Free eStatements

- Priority service at branches for salary account holders

- Corporate partnership benefits specific to your employer’s arrangement with Sampath

Honest Assessment

Dilini, a marketing manager earning Rs. 75,000 at an advertising agency in Colombo, used to spend two hours every month standing in line at her previous bank to pay utility bills, request statements, and manage her credit card. After switching to Sampath Salary Plus, she does all of that from the Vishwa app in 10 minutes on a Sunday evening while watching Netflix. When she needed a personal loan for a kitchen renovation, she applied through the app, got approval within 48 hours, and never set foot in a branch. Her previous bank would have taken two weeks and three branch visits.

Strengths: Best mobile banking app in Sri Lanka (Sampath Vishwa), contactless payments via PayZ and WePay, loan applications entirely through the app, salary advance from your phone, QR payments at 100,000+ merchants, 12 super branches for premium in-person service.

Weaknesses: Smaller physical branch network (229 branches) than state banks. OD capped at 2x salary (HNB offers 3x). Credit card cashback and perks are average; DFCC and Commercial Bank offer better card-linked benefits. If you live in a rural area with limited internet connectivity, the app-first approach is less useful.

Pick Sampath if: You are a digital-first person who wants to do everything from your phone. The Vishwa app is the single best banking app in Sri Lanka, and the salary account is the gateway to that ecosystem. Skip Sampath if: You need maximum OD borrowing power (go HNB), the best credit card perks (go DFCC), or rural branch coverage (go BOC or People’s Bank).

If you are comparing card benefits, also check our best credit card in Sri Lanka guide for standalone credit card options that you can pair with any salary account.

What Is the Best Salary Account for Government Employees in Sri Lanka?

Bank of Ceylon Salary salary savings account Sri Lanka

Bank of Ceylon Salary salary savings account Sri Lanka

The BOC Smart Salary Saver is the best salary savings account for government and semi-government employees in Sri Lanka. With 660+ branches across all 25 districts, up to 90% salary advance after just 3 months, an exclusive Affinity Credit Card for state sector workers, and a minimum salary requirement of just Rs. 25,000, BOC offers accessibility that no private bank can match.

Bank: Bank of Ceylon

Account Name: BOC Smart Salary Saver

Best For: Government and semi-government employees, workers who prefer state bank security

Age: 18 to 55 years

Initial Deposit: Rs. 2,000

BOC is Sri Lanka’s largest state-owned bank, with Rs. 5.3 trillion in total assets and over 25% of system-wide banking assets. If you work in the government or semi-government sector, BOC likely already processes your salary. The Smart Salary Saver was launched during BOC’s 82nd anniversary specifically to serve permanent employees across government, semi-government, private sector, and qualified professionals. You must be an EPF member or pension scheme participant.

Account Structure and Interest

Unlike most salary accounts, the BOC Smart Salary Saver does not pay interest directly on your balance. Instead, funds above Rs. 10,000 are automatically swept daily into a linked Fund Management Account (FMA) that earns a return. When you withdraw or make payments that exceed your account balance, the deficit is automatically funded back from the FMA. The exact FMA rate is not publicly listed; you need to call BOC’s 24-hour hotline (1975) to confirm the current rate. This sweep structure means your idle money works harder than in a standard savings account, but the lack of transparency on the rate is a drawback.

Salary Advance (BOC’s Standout Feature)

BOC offers one of the most generous salary advance facilities in Sri Lanka:

- Up to 90% of take-home salary available as an advance

- Qualifying period: 3 consecutive months of salary remittance

- Tenure: 6 months, with repayment through monthly salary on a revolving basis

- Available to all eligible account holders (government, semi-government, private sector, professionals)

That 90% figure is significantly higher than most competitors. DFCC offers 50%, Sampath offers a similar range, and NTB does not publicly advertise a percentage. For a government employee earning Rs. 60,000, that is Rs. 54,000 available before payday; enough to cover a medical emergency, school fees, or an unexpected home repair without touching a credit card.

Credit Card Benefits

BOC offers a full range of credit cards to salary customers:

Card terms:

- Joining fee: Free

- Annual fee: First year waived (subsequent years vary by tier)

- Interest rate: 2.16% per month (25.92% p.a.) on unpaid balances

- Interest-free period: 22 to 52 days

- 0% installment plans: Up to 24 months for education, hospital, automobile, insurance, home appliances, and solar

- Travel insurance: Free cover up to USD 250,000 for cards with limits of Rs. 250,000+

- Rewardz Plus loyalty programme: Automatic enrollment, earn points on every POS and online transaction, redeem for e-vouchers, flights, hotels, electronics, and movie tickets at rewardzplus.boc.lk

BOC Affinity Credit Card (State Sector Exclusive)

This is BOC’s exclusive card for government employees, and it is not available at any other bank:

- Free joining fee and first-year annual fee waiver

- Zero-interest installment facility at BOC merchant network

- Emergency hospitalization limit enhancement (your credit limit is temporarily increased for hospital bills)

- 50% cash advance on available credit limit, once per month, at any ATM

- Easy settlement plans up to 24 months

- Exclusive discount promotions through BOC merchant partners

BOC also offers profession-specific cards: a State Sector Card, Doctors’ Card (requires SLMC ID), and Chartered Accountants’ Card (requires CA Sri Lanka ID). If you are a government doctor or CA, these specialty cards give you benefits tailored to your profession.

Loan Benefits

- 0.5% interest rate concession on leasing and personal loans for Smart Salary Saver holders

- Housing loan: From 10% interest rate, up to Rs. 100 million, repayment up to 25 years

- Personal loan and vehicle leasing: Competitive rates with the 0.5% concession applied

For context, competitor housing loan rates are: Commercial Bank 11.50-14.50%, People’s Bank 12-14.5%, HNB 12.50-17%. BOC’s “from 10%” starting rate is among the lowest in the market, and the 0.5% salary account concession makes it even more competitive. If you are planning to buy a house or apartment, the loan rate alone could justify choosing BOC.

Digital Banking

BOC has significantly upgraded its digital offering in 2025 with three platforms:

BOC Flex (launched March 2025, newest app):

- Self-registration without visiting a branch

- Biometric authentication (fingerprint/face)

- Fund transfers (one-to-one, multiple, scheduled)

- Bill payments, QR payments (LANKAQR certified)

- Open savings accounts and fixed deposits with renewal options

- Instant loans against fixed deposits

- Customizable widgets, expense tracker, payment reminders

- Supports LankaPay Online Payment Platform (LPOPP)

- Government Digital Payment Platform (GDPP) for offline payments

BOC SmartPay (QR Payments):

- First Sri Lankan app certified as LANKAQR by the Central Bank

- Peer-to-peer fund transfer between any banks

- Scan and pay at 100,000+ LANKAQR-certified merchant outlets islandwide

- Accepts China UnionPay QR payments

Additional digital features:

- NFC-enabled electronic debit card (contactless payments, e-commerce enabled)

- Smart Passbook (digital passbook replacing physical)

- SMS alerts and e-statements

- BOC Smart Online Banking (web-based)

- Automated monthly bill payment facility

Branch and ATM Network (BOC’s Killer Feature)

No bank in Sri Lanka comes close to BOC’s physical reach:

BOC processes 9.17 million ATM/CRM transactions per week, totaling Rs. 212 billion (April 2025 data). The bank holds over 5 million active debit cardholders, roughly 26% of all active debit cards in Sri Lanka. Monthly debit card transaction volume is Rs. 20 billion at merchants and Rs. 300 billion at ATMs.

If you live or work outside Colombo, this network is the deciding factor. In Kilinochchi, Mullaitivu, or Monaragala, BOC likely has a branch within walking distance when no private bank does.

Honest Assessment

Tharindu, a school principal in Polonnaruwa, was paying Rs. 1,200 per year in debit card fees and another Rs. 3,500 in credit card annual fees at a private bank branch that was 45 minutes from his school. When he switched to BOC Smart Salary Saver, he got a free debit card, free first-year credit card, and a salary advance of up to 90% when his wife needed emergency dental surgery during a month when the family budget was already stretched thin. The BOC branch was a 10-minute walk from the school.

Strengths: Unmatched physical reach (660+ branches, 2,300+ touchpoints), 90% salary advance (highest among competitors), exclusive Affinity Card for government workers, competitive housing loan rates starting at 10%, LANKAQR support at 100,000+ merchants.

Weaknesses: The FMA interest structure is not transparent; you cannot easily compare rates without calling the bank. The digital experience through BOC Flex is catching up but still lags behind Sampath Vishwa and ComBank Digital in user interface polish. The credit card annual fees after year one are not clearly published online. No bundled life or accident insurance with the salary account itself.

Pick BOC if: You are a government or semi-government employee, you work outside the Western Province, or you value physical branch access above everything else. Skip BOC if: You are a private sector employee earning above Rs. 50,000 and want better credit card cashback, a more polished app, or a transparent interest rate structure. DFCC or Commercial Bank will serve you better.

Which Salary Account Is Best for Building Wealth in Sri Lanka?

NDB Salary Max salary savings account Sri Lanka

NDB Salary Max salary savings account Sri Lanka

NDB Salary Max combines salary banking with investment products, making it the best salary savings account for employees who want to grow their money beyond basic savings. After 3 consecutive salary remittances, you qualify for a salary advance or POD equal to your monthly salary, plus attractive rates on Dream Maker personal loans. NDB’s real differentiator is the integrated wealth management arm through NDB Wealth, giving salary customers a direct pathway to unit trusts, money market funds, and structured investment products.

Bank: NDB Bank

Account Name: NDB Salary Max Savings Account

Best For: Employees who want to combine salary banking with investment products

Minimum Salary: Rs. 35,000 net per month

NDB Bank (formerly National Development Bank) started as a development finance institution and retains a strong investment DNA. This heritage shows in the Salary Max product, which is designed not just for day-to-day banking but for building long-term wealth. NDB Wealth Management, the bank’s investment arm, manages over Rs. 100 billion in assets and is one of the largest fund management companies in Sri Lanka.

Salary Threshold and Eligibility

- Minimum net salary: Rs. 35,000 per month

- Corporate salary arrangement required

- Zero balance account opening for salary customers

- Salary must be credited within 30 days of account opening

- Available to permanent employees in private and public sector

Salary Advance and POD (NDB’s Key Benefit)

After remitting your salary for 3 consecutive months, you qualify for:

- Salary advance or POD (Pre-approved Overdraft) equal to your monthly salary

- Quick access through branch or NEOS app

- Repaid from subsequent salary credits on a revolving basis

- Dream Maker personal loan at attractive interest rates for larger borrowing needs

The salary advance qualifying period of just 3 months is competitive. BOC also requires 3 months, while HNB and Seylan may require up to 6 months depending on the corporate arrangement. NDB’s advance equals your full monthly salary (1x), which is on par with most competitors.

Credit Card Benefits

NDB offers credit cards to Salary Max customers with waived fees:

- NDB Visa Classic / Mastercard: Entry-level card for salary customers

- NDB Visa Gold / Mastercard Gold: For higher earners

- NDB Visa Platinum: Premium tier with enhanced benefits

- Joining fee: Waived for salary customers

- Annual fee: First year free

- Installment plans: 0% plans available at NDB partner merchants

- NDB Rewards programme: Earn points on card transactions

- Supplementary cards: Free for family members

NDB’s credit card offering is standard but unremarkable. You get a free card with waived fees, but the cashback rates and merchant partnerships are not as extensive as DFCC or Commercial Bank. The card is a nice addition to the salary account, but it is not the reason to choose NDB.

Overdraft Facility

- Available after qualifying salary credits (typically 3-6 months)

- Limit based on salary and employer arrangement

- Interest charged daily on the amount utilized

- Unsecured facility (no collateral needed)

NDB does not publicly advertise a specific OD multiple like HNB’s 3x or DFCC’s 2x. The limit is determined case by case based on your salary level and employer relationship. This means you may get a generous OD if you are a high earner at a blue-chip company, but less certainty if you are mid-range.

Loan Benefits

NDB offers preferential rates for Salary Max holders on:

- Dream Maker Personal Loan: NDB’s flagship personal loan product with attractive rates for salary customers; faster approval for Salary Max holders

- Housing loans: Competitive rates with longer tenures (up to 25 years)

- Vehicle loans/leasing: Special packages for salary account holders

- Education financing: Available for higher education (local and overseas)

- Gold-backed loans: Available for salary customers with gold assets

The Dream Maker brand is NDB’s consumer lending flagship. Salary Max customers get priority processing and preferential rates on Dream Maker loans, which is a genuine advantage if you plan to borrow for a major purchase within the next few years.

NDB Wealth Management (NDB’s Differentiator)

This is what makes NDB unique among salary account providers. NDB Wealth Management offers:

Unit Trusts and Money Market Funds:

- NDB Wealth Money Fund (money market fund for short-term parking)

- Equity funds for long-term growth

- Income funds for regular payouts

- Minimum investment thresholds accessible for salary earners

Fixed Deposit Integration:

- Higher FD rates for salary account holders

- FD ladder strategies managed through a single relationship

- Automatic FD renewal and maturity alerts

Wealth Advisory Services:

- Available for customers maintaining higher balances

- Portfolio review and investment planning

- Tax-efficient investment strategies

- Retirement planning guidance

For a salary earner who wants to do more than just save, this integration matters. At most banks, opening a unit trust account requires a separate application, separate KYC, and a separate relationship. At NDB, your Salary Max relationship gives you direct access to the wealth management arm. You can start with Rs. 10,000 in a money market fund and scale up as your income grows.

Digital Banking: NDB NEOS

NDB NEOS Mobile App:

- Fund transfers (own accounts, third-party, interbank)

- Bill payments and utility payments

- QR code payments (LANKAQR certified)

- Fixed deposit opening and management

- Loan applications and tracking

- Credit card management

- Account statements and transaction history

- Biometric login

- Push notifications

NDB Internet Banking (Web):

- Full banking functionality for desktop users

- Statement downloads and certificate requests

- Standing order management

NDB NEOS is a competent banking app that handles all essential functions. It does not match Sampath Vishwa’s polish or feature depth, but it is reliable and covers the basics well. The FD management features are particularly useful for the wealth-building use case.

Branch and ATM Network

NDB has the smallest physical network among the banks covered in this guide. With 115+ branches, it is roughly half the size of Sampath (229) and a fraction of BOC (660+). The branches are concentrated in Colombo, other major cities, and commercial centres. If you work in a tier-1 city, NDB access is fine. If you are in a rural area, you will rely heavily on the NEOS app and interbank ATM access (with fees).

Unique Perks

- Investment integration: Direct access to NDB Wealth unit trusts and advisory

- Higher FD rates for salary relationship customers

- NDB Rewards programme on card transactions

- Free SMS alerts and eStatements

- Priority banking service at branches for qualifying salary customers

Honest Assessment

Chaminda, a software engineer earning Rs. 150,000, kept his salary at a large bank for five years. He had Rs. 800,000 sitting idle in a savings account earning 2.5% interest. When his colleague introduced him to NDB Salary Max, he moved his salary and within three months had a salary advance facility, a free credit card, and most importantly, his wealth manager at NDB helped him set up a FD ladder (Rs. 100,000 per month for 12 months at staggered maturities) combined with Rs. 50,000/month into the NDB Wealth Money Fund. After one year, his combined return was significantly higher than the flat savings rate he was earning before, and he had liquidity every month from maturing FDs.

Strengths: Integrated wealth management through NDB Wealth (unit trusts, money market funds, advisory), competitive FD rates for salary customers, Dream Maker personal loan with preferential rates, 3-month qualifying period for salary advance, investment-first positioning unique among Sri Lankan salary accounts.

Weaknesses: Smallest branch and ATM network of any bank in this guide (115+ branches). No publicly advertised OD multiple, so borrowing power is uncertain until you apply. Credit card perks are average. The app is functional but not market-leading. If you do not plan to invest beyond basic savings, NDB’s key differentiator is wasted on you.

Pick NDB if: You earn above Rs. 75,000 and want a salary account that doubles as your investment platform. The wealth management integration is genuinely unique and gives you access to professional investment products without opening separate accounts. Skip NDB if: You need a wide branch network, maximum OD borrowing power, or best-in-class credit card perks. Go BOC for branches, HNB for OD, or DFCC for cards.

7. People’s Bank Jana Jaya Salary Account (Widest Branch Coverage)

People’s Bank Salary salary savings account Sri Lanka

People’s Bank Salary salary savings account Sri Lanka

Bank: People’s Bank

Account Name: Jana Jaya Savings Account (salary-linked)

Best For: Government and semi-government sector employees, plantation workers, and anyone in rural Sri Lanka who needs maximum branch access

Why Consider: Second-largest branch network in the country (700+) and the only bank with deep penetration into plantation and rural areas

People’s Bank is Sri Lanka’s second-largest state bank with over 700 branches, making it the most accessible bank for workers outside Colombo and the Western Province. The Jana Jaya account is their savings product for salaried employees, self-employed individuals, and professionals with a steady monthly income.

Account Details

- Minimum opening deposit: Rs. 2,000 at any People’s Bank branch

- Interest rate: 2.50% p.a. (effective May 2026)

- Savings options: Flexible daily, weekly, or monthly contributions

- Designed for salaried employees, self-employed, or professionals with steady income

Credit Card and Debit Card

- Free People’s Bank Debit Card with ATM access across the entire 700+ branch network

- Credit card facilities available for salary customers, though People’s Bank’s card products are less feature-rich than private banks

- No publicly disclosed cashback or rewards programme specific to salary customers

Loan Benefits

- Special loan facilities at preferential rates for Jana Jaya account holders

- Personal loans, housing loans, and vehicle loans with priority processing for salary customers

- People’s Bank is a major lender for government sector housing loans, often offering the lowest rates in the market for state employees

Digital Banking

- People’s Wave mobile app (iOS and Android): Fund transfers, bill payments, balance inquiries, and account management

- Internet banking and voice banking app

- QR payment capability via the LANKAQR network

The digital experience is functional but not competitive with Sampath Vishwa or NTB’s FriMi. People’s Bank is investing in digital transformation, but as of 2026, the app is adequate for basic transactions rather than a comprehensive digital banking platform.

Branch and ATM Network (People’s Bank’s Killer Feature)

- 700+ branches across all 25 districts, including rural, semi-urban, and plantation areas

- ATMs at every branch location plus standalone ATMs

- People’s Leasing and Finance (subsidiary) adds further touchpoints

- Access to the LankaPay ATM network for broader coverage

For context, People’s Bank has branches in locations where no private bank operates. Tea estate workers in Nuwara Eliya, rubber plantation workers in Ratnapura, and fishing community members in Trincomalee all have People’s Bank access. If you work in a rural area, People’s Bank might be your only option, and it is a solid one.

Unique Perks

- Festival advance facility: A small cash advance before Sinhala/Tamil New Year and Christmas, helping employees manage seasonal expenses. No other bank offers this systematically.

- Special offers for overseas travel through People’s Travels (Pvt) Ltd, the bank’s travel subsidiary

- Strong integration with government payroll systems for seamless salary processing

- Accounts accessible at 700+ branches means you can transact anywhere in Sri Lanka without worrying about finding your bank

Dinesh works as a teacher in Anuradhapura. His salary of Rs. 65,000 per month goes into a People’s Bank Jana Jaya account because there is literally no DFCC or HNB branch within 30 kilometres of his school. Every April, the festival advance gives him Rs. 15,000 before the Sinhala New Year without touching his savings. When he needed a personal loan for his daughter’s tuition, People’s Bank approved it in five days using his salary history. The interest rate was not as low as what DFCC advertises, but the convenience of doing everything at the branch next to his school made the difference.

Honest Assessment: People’s Bank mirrors BOC in strengths and weaknesses. The branch network is unmatched for rural access. Government and semi-government employees get streamlined salary processing and loan approvals. The festival advance is a genuinely useful and unique perk.

But the interest rate (2.50%) is one of the lowest in this guide. Credit card and cashback benefits are minimal compared to DFCC, HNB, or Commercial Bank. The digital banking experience lags behind private banks. And the overdraft facility is less transparent than competitors who publish their OD multiples publicly. For private sector employees earning Rs. 50,000+ who live in an urban area, DFCC Salary Partner or HNB Salary Smart offer significantly better value. People’s Bank is the right choice when accessibility matters more than premium benefits.

8. Seylan Bank Accelerate Salary Savings (Best Interest-Free Salary Advance)

Seylan Bank Salary salary savings account Sri Lanka

Seylan Bank Salary salary savings account Sri Lanka

Bank: Seylan Bank

Account Name: Seylan Accelerate Salary Savings Account

Best For: Mid-level private sector employees who want an interest-free salary advance facility

Why Consider: Only bank in Sri Lanka offering a confirmed interest-free salary advance for qualifying tiers

Seylan’s Accelerate account is their salary-focused savings product, and it comes with four distinct tiers based on your monthly salary routing, similar to DFCC’s tiered approach.

Seylan Accelerate Salary Tiers

Interest Rates

Accelerate pays slightly better than Seylan’s standard savings account:

Standard Seylan savings caps at 2.50% for Rs. 10,000+, so Accelerate gives you 0.50% extra at the Rs. 50,000+ tier. Not a game-changer, but better than nothing.

Credit Card Benefits

Seylan offers 8 credit card products, and salary account holders get a first-year annual fee waiver on all cards. The cards worth knowing about:

- Visa Gold (Rs. 150,000 min income): Credit limit Rs. 75,000 – Rs. 199,000, basic rewards

- Visa Platinum (Rs. 150,000 min income): Credit limit Rs. 200,000 – Rs. 999,000, earns 1 reward point per Rs. 300 spent (minimum Rs. 1,000 transaction)

- Visa Signature (Rs. 300,000 min income): Credit limit Rs. 1,000,000+, earns 1 point per Rs. 100 spent

- Visa Infinite Metal (by invitation only): Free for life with no annual or joining fees, Lounge Key access to 1,100+ airport lounges (first visit per year free), 30-day travel insurance, Visa Concierge service, NFC contactless

Interest rate across all cards is 26.00% p.a. with up to 51 days interest-free. Foreign transaction markup is minimum 4.50%, which is higher than most competitors.

Interest-Free Salary Advance (Seylan’s Differentiator)

This is what makes Seylan Accelerate stand out. Prime and Premier tier customers get access to an interest-free salary advance facility. Unlike HNB’s overdraft (which charges interest) or DFCC’s OD (also interest-bearing), Seylan’s advance costs you zero in interest.

Eligible customers are automatically registered and notified by email. The exact percentage of salary available as an advance is not publicly disclosed and is extended on a selective basis. You need to be in the Prime (Rs. 150,000+) or Premier (Rs. 300,000+) tier to qualify.

Loan Rates

Accelerate holders are marketed as getting “attractive interest rates,” which likely means the lower end of these ranges, but Seylan does not publicly confirm the exact preferential discount.

Digital Banking

- App: Seylan Mobile Banking (iOS and Android), available in English, Sinhala, and Tamil

- Features: Biometric login (Face ID, fingerprint), fund transfers to Seylan and other banks, bill payments, credit card settlement, open savings accounts and FDs in-app, branch/ATM locator, 3 OTP options (SMS, email, soft token)

- SeylanPay: Separate digital payments app for merchants and QR payments

Branch and ATM Network

- 170-173 branches across Sri Lanka

- 210-216 ATMs plus 102 cash recycler machines

- 70 cash deposit machines and 66 cheque deposit machines

Seylan’s physical network sits between the private bank leaders (Commercial Bank at 900+ ATMs) and smaller players (NTB at 99 ATMs). Decent coverage but not the widest.

Unique Perks

- Seylan Mega Rewards: Maintain a minimum Rs. 20,000 balance for 6-12 consecutive months for bonus rewards

- Merchant offers: Up to 15% cashback at Cargills every Saturday, 10% off at select retail partners

- Trilingual app support (rare among Sri Lankan banking apps)

Honest Assessment: Seylan Accelerate’s interest-free salary advance is its genuine differentiator. No other bank explicitly offers a zero-interest advance on your salary. But the catch is transparency: Seylan does not disclose the exact advance percentage or qualifying criteria publicly, and you need to be earning Rs. 150,000+ to access it. The savings interest rate (3.00% max) is low, the credit card rewards are weaker than DFCC’s 1% cashback, and the 4.50% foreign transaction fee is steep. Customer reviews on ReviewSriLanka rate Seylan at 2.2 out of 5, with complaints about branch service quality and waiting times. If your employer banks with Seylan and you earn Rs. 150,000+, the interest-free advance makes it worth staying. Otherwise, DFCC or HNB offer better overall value.

9. Nations Trust Bank Inner Circle (Best for Lifestyle and Insurance Perks)

Nations Trust Bank salary savings account Sri Lanka

Nations Trust Bank salary savings account Sri Lanka

Bank: Nations Trust Bank

Account Name: Nations Salary Saver + Inner Circle Membership

Best For: Professionals earning Rs. 100,000+ who want insurance coverage, lifestyle banking, and premium credit cards bundled into one relationship

Why Consider: Only salary account in Sri Lanka that includes life insurance (6 months’ salary) and health cover (Rs. 100,000) at no extra cost

NTB uses a two-layer approach. You open a Nations Salary Saver account, and if you meet the threshold, you unlock Inner Circle membership, which is where the real benefits live.

How to Qualify for Inner Circle

For higher-tier Salary Saver benefits without Inner Circle, the threshold jumps to Rs. 200,000 net salary per month.

Credit Card Benefits (Inner Circle’s Strength)

Inner Circle members get two free credit cards with annual fees waived:

American Express Platinum Card:

- Annual fee: Rs. 7,500 (waived for Inner Circle)

- 1 Membership Reward point per Rs. 100 spent (points never expire)

- Redeemable for FlySmiLes, Cathay Pacific Asia Miles, Hilton Honors

- Complimentary travel insurance up to USD 200,000

- 0% installment plans for 6 and 12 months

- Global concierge service

World Mastercard Credit Card:

- Also provided free to Inner Circle members

- Wider merchant acceptance than Amex in Sri Lanka

Other NTB Amex cards available separately include the Explorer (Rs. 22,500/year, 2x miles on travel, Priority Pass with 4 free lounge visits) and the SriLankan Airlines Platinum Amex (1 FlySmiLes mile per Rs. 200, companion ticket benefit).

Interest rate across all cards: 26% p.a. Fuel surcharge: 2% on Amex, 1% on Mastercard.

Insurance Benefits (Unique to NTB)

This is where NTB beats every other salary account in Sri Lanka:

No other Sri Lankan bank bundles life insurance and health cover into a salary account at zero cost. DFCC, HNB, and Commercial Bank do not offer this.

Pre-Approved Lease

Inner Circle members get a pre-approved vehicle lease of up to Rs. 2,000,000. No separate application process needed; the approval is built into your membership.

Overdraft and Loans

- Preferential overdraft rates confirmed as an Inner Circle benefit, but exact limits and rates are not publicly disclosed

- Preferential interest rates on personal, housing, and automobile loans (also undisclosed publicly; described as “reduced and preferential”)

- Preferential FD rates for Inner Circle members

Digital Banking: FriMi

NTB’s FriMi app is arguably the most innovative digital banking platform in Sri Lanka:

- Fully digital onboarding: Open an account without visiting a branch (physical Mastercard debit card delivered to your door)

- LANKAQR payments at any merchant

- Savings Pot: Auto-save for regular expenses

- Round Up Savings: Automatically rounds up transactions to the nearest Rs. 50, 100, or 500 and saves the difference

- Bucket List Savings: Goal-based savings with target tracking

- In-app marketplace: Doctor channeling, concierge, grocery shopping, gaming

- Biometric security, instant card block/unblock, transaction limit controls

NTB also offers separate Internet Banking and SMS Banking, all free for Inner Circle members.

Branch and ATM Network

- 96 branches (smallest among major Sri Lankan banks)

- 99 ATMs plus 64 cash deposit and withdrawal machines

- Access to 3,700+ ATMs via the LankaPay network

- Mobile ATMs visiting neighborhoods in underserved areas

Unique Perks

- Bank-At-Your-Doorstep: A dedicated relationship manager visits you at home or office

- Dedicated service counters at all NTB branches island-wide

- Fee waivers on leasing, foreign currency transactions, and most banking services

- Exclusive merchant offers: dining discounts, hotel stays, Mastercard travel offers

Priya is a marketing manager earning Rs. 130,000 a month. She switched to NTB’s Inner Circle after her father was hospitalized with a heart condition. The Rs. 100,000 critical illness health cover kicked in within two weeks. She later discovered the Salary Guard benefit: if anything happened to her, her family would receive six months of her salary automatically. No claim forms, no waiting period. For Priya, the insurance benefits alone justified the switch from her previous bank, where she had been paying Rs. 15,000 a year for a separate health insurance policy with lower coverage.

Honest Assessment: NTB Inner Circle is the best salary account in Sri Lanka if insurance and lifestyle benefits matter more to you than raw cashback or overdraft limits. The Salary Guard and health cover are genuinely unique. FriMi is best-in-class for digital UX. The free Amex Platinum card is a premium product.

But the downsides are real. NTB has the smallest branch network of any major Sri Lankan bank (96 branches vs Seylan’s 170+, BOC’s 600+). The Salary Saver interest rate is only 2.00%, one of the lowest. American Express acceptance at Sri Lankan merchants is more limited than Visa or Mastercard. And the preferential loan and overdraft rates lack publicly disclosed numbers, so you are negotiating blind. The Rs. 100,000 gross salary minimum also locks out most entry-level workers. If you earn Rs. 100,000+ and live in an urban area, NTB Inner Circle is a strong contender. If you need wide branch access or earn below Rs. 100,000, look at DFCC or BOC instead.

Is NSB the Safest Bank for Salary Savings in Sri Lanka?

NSB iSaver salary savings account Sri Lanka

NSB iSaver salary savings account Sri Lanka

NSB (National Savings Bank) is the only bank in Sri Lanka where all deposits carry a 100% government guarantee under the National Savings Bank Act. This is not the same as the Rs. 600,000 deposit insurance that covers private banks. NSB’s guarantee covers your entire balance, no cap. That makes it the safest place to park money in Sri Lanka, full stop.

Bank: National Savings Bank

Account Name: NSB Savings Accounts (Ordinary, Premier, Neo, Happy Savings)

Credit Rating: (LRA) AAA Stable, the highest possible in Sri Lanka

Best For: Conservative savers who prioritize safety, higher interest rates, and government-backed security over salary-linked perks

Important distinction: NSB does not offer a traditional “salary savings account” product like DFCC, HNB, or Commercial Bank. There is no salary-linked credit card, no overdraft against salary, no salary advance facility. NSB is a specialized savings bank, not a full-service commercial bank. You come to NSB for safety and rates, not for salary perks.

Interest Rates (NSB’s Real Advantage)

NSB consistently pays higher savings interest than private banks:

Compare NSB’s 6.75% Premier rate to Seylan Accelerate’s 3.00% or NTB’s 2.00%. If you have Rs. 1,000,000+ in savings, NSB pays you more than double what most private banks offer.

Fixed Deposit Rates (Best in Market)

The Abhiman Samarum FD at 9.25% for 24 months is the highest FD rate among all banks covered in this guide. If you are building a fixed deposit ladder, NSB should be your first stop.

NSB EASY Card (Credit Facility Against FDs)

NSB does not offer a traditional credit card. Instead, they offer the NSB EASY Card, a Mastercard credit facility secured against your fixed deposits:

- Annual fee: None

- Late payment fee: None

- Excess limit fee: None

- Stamp duty: None

- Interest rate: Only 3% above your FD rate (applied only on the amount you withdraw, from the date of withdrawal)

- Credit limit: Up to 80% of your FD value, maximum Rs. 1,000,000

- Eligibility: FD held for 12+ months, age 18+

- Can link up to 10 NSB accounts to one card

- Accepted at all Mastercard merchants worldwide and all NSB ATMs

This is essentially a zero-fee overdraft against your FD. If your FD earns 7.25% and you borrow against it at 10.25% (7.25% + 3%), you are paying just 3% net for short-term credit. No other bank offers this structure.

Digital Banking

- NSBPay app (iOS and Android): Self-registration, biometric and PIN login, QR payments (static and dynamic), fund transfers, utility bill settlement, balance inquiry, account history, foreign exchange rates, recurring bill payments

- Tap & Go: Sri Lanka’s first in-app contactless payment via Mastercard tokenization. Pay at any contactless terminal directly from your phone without a physical card

- NSB Online Banking at digital.nsb.lk

Branch and ATM Network (Massive Reach)

- 262 branches across all provinces

- 417 ATMs and cash recycler machines

- 4,006 postal agents in rural areas

- 16,000 iSaver deposit retailers (deposit up to Rs. 5,000/day via mCash retailers)

- Total physical touchpoints: over 20,000

That 20,000+ touchpoint network is unmatched. If you live in a rural area where private banks have no presence, NSB likely has a postal agent or iSaver retailer within walking distance.

Loan Products

- Housing loans (promotional rates as low as 7% p.a. historically)

- First Home Owner loans

- Auto loans

- Education loans (NSB Buddhi)

- Speed Loans (against deposits)

- Gold pawning (Ran Sahana)

Exact current rates are not listed publicly on the website, but NSB’s government-backed status typically translates to competitive rates.

The Two-Account Strategy

Amal is a software developer earning Rs. 95,000 a month. He routes his salary to a DFCC Salary Partner account for the credit card, cashback, and overdraft. But every month, he transfers Rs. 30,000 to his NSB Premier Savings account where it earns 6.75% interest with a full government guarantee. His emergency fund of Rs. 500,000 sits in NSB because he knows it is the only bank in Sri Lanka where he cannot lose a single rupee, regardless of what happens to the banking sector. When he needed short-term cash, he used the NSB EASY Card against his FD at just 3% above the FD rate instead of taking a personal loan at 15%+.

This two-account approach, salary perks at a private bank plus safety and rates at NSB, is the optimal strategy for most Sri Lankan workers.

Honest Assessment: NSB is not a salary account. It is a savings fortress. You will not get credit card cashback, salary advances, overdraft facilities, or a dedicated relationship manager. The digital experience is improving (Tap & Go is genuinely innovative), but customer service reviews are poor, with reports of long queues, staff unaware of advertised products, and ATMs that frequently malfunction. Branch processes are slow with government-bank bureaucracy. But none of that matters if your goal is maximum safety and maximum interest. NSB’s 100% government guarantee and AAA credit rating make it the only truly risk-free savings option in Sri Lanka. Use it as your savings and FD bank, not your primary transaction bank.

Should You Open an International Bank Salary Account in Sri Lanka?

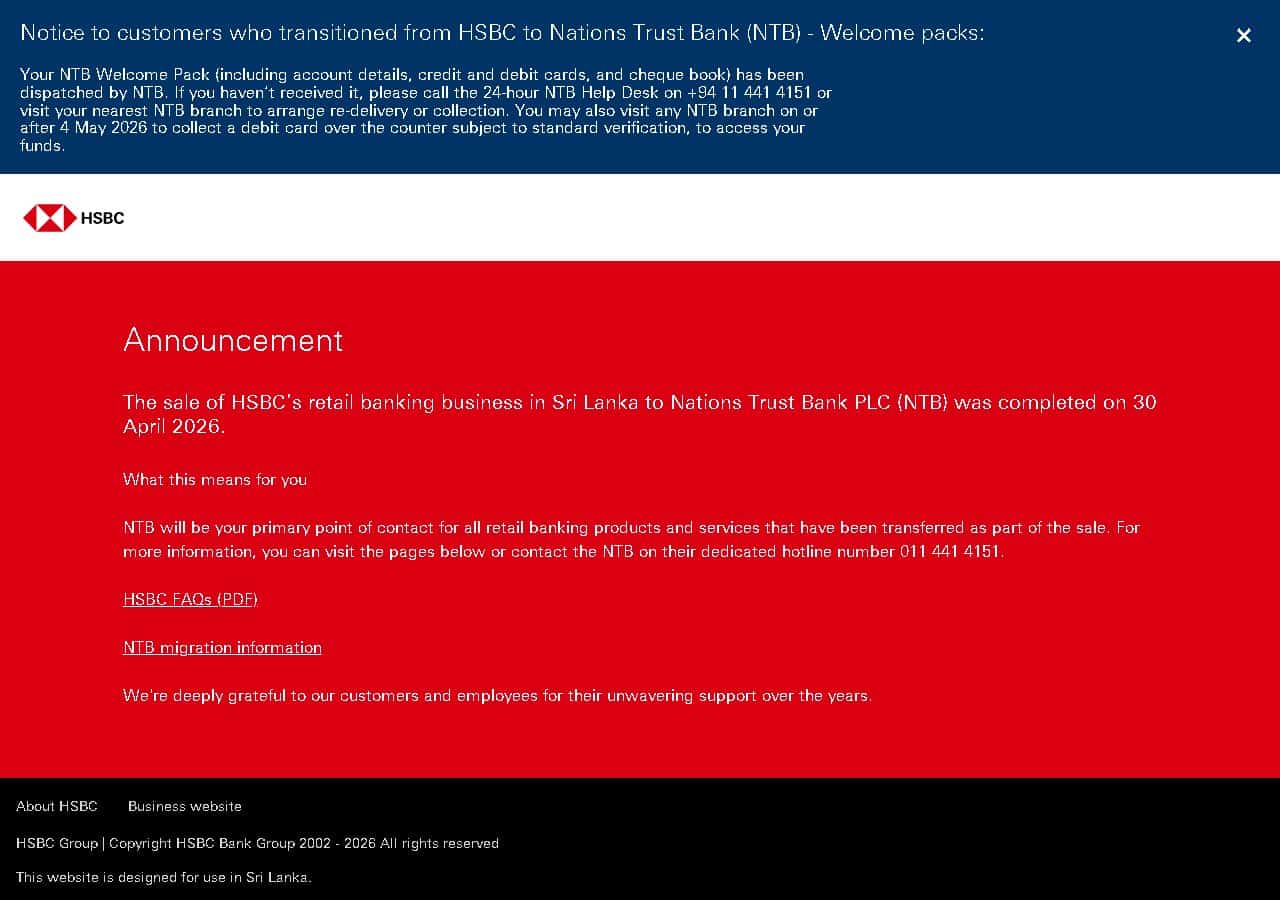

Only if you work for a multinational company, earn Rs. 500,000+ per month, and need international banking features that local banks cannot provide. After HSBC’s exit, Standard Chartered is the only international bank still offering retail salary accounts in Sri Lanka.

HSBC Sri Lanka (No Longer Available for New Accounts)

HSBC Sri Lanka salary savings account Sri Lanka

HSBC Sri Lanka salary savings account Sri Lanka

Status: HSBC completed the sale of its retail banking business in Sri Lanka to Nations Trust Bank (NTB) on April 30, 2026. HSBC no longer offers retail banking products, including salary accounts, credit cards, or personal loans in Sri Lanka.

If you were an HSBC salary account holder, your account has been migrated to Nations Trust Bank. NTB’s dedicated HSBC migration helpline is +94 11 441 4151. All HSBC retail banking products (savings accounts, credit cards, personal loans) are now serviced by NTB.

What this means for salary account seekers: HSBC is no longer an option. If you wanted international banking, Standard Chartered is now your only choice among foreign banks in Sri Lanka. Alternatively, NTB Inner Circle (which now inherits HSBC’s customer base) offers some international features through the American Express card partnership.

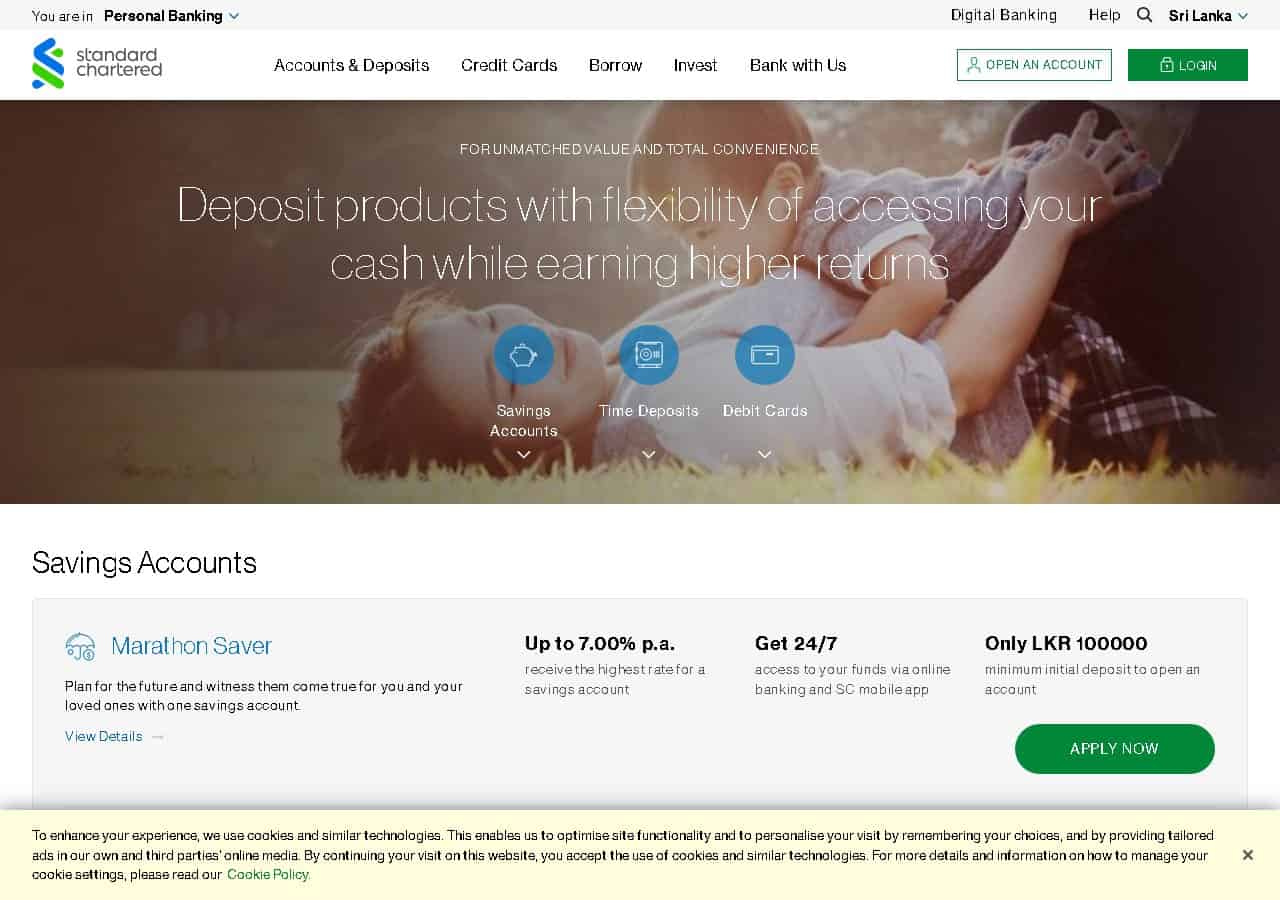

Standard Chartered Sri Lanka Employee Banking (Only International Bank Option)

Standard Chartered SL salary savings account Sri Lanka

Standard Chartered SL salary savings account Sri Lanka

Bank: Standard Chartered Sri Lanka

Account Name: Standard Chartered Employee Banking / Priority Banking

Best For: High-earning professionals at multinational companies who need international banking connectivity and premium rewards

Why Consider: The only international bank still offering retail salary accounts in Sri Lanka after HSBC’s exit

With HSBC gone, Standard Chartered is now the sole international bank operating in the Sri Lankan retail banking market. Their Employee Banking program targets corporate employees at partner companies, while Priority Banking serves high-net-worth individuals.

Eligibility Tiers

That Rs. 500,000 threshold is the highest of any bank in this guide. This is premium banking for senior executives and expatriates, not for the average salaried worker.

Credit Card: 360° Rewards Programme

Standard Chartered credit cards come with the 360° Rewards programme, automatically enrolled at no extra cost:

- Journey Credit Card: 1 reward point per Rs. 100 spent on travel-related merchants

- Rewards Credit Card: Points on all retail spending, redeemable for shopping, dining, and travel

- Points never expire

- 0% installment plans at select merchants

- Redemption through the dedicated 360° Rewards platform at scb360rewards.lk

The rewards structure is points-based rather than direct cashback. Unlike DFCC’s straightforward 1% cashback, Standard Chartered requires you to accumulate and redeem points, which adds friction.

Priority Banking Benefits

- Dedicated Relationship Manager for personalized banking

- Priority service at all Standard Chartered Sri Lanka branches

- Preferential foreign exchange rates for international transfers and remittances

- Preferential interest rates on deposits and loans

- International banking connectivity across Standard Chartered’s presence in 50+ markets

- Airport lounge access through premium credit card programs

- Wealth management and investment advisory services

- Free SC Mobile Banking with international transfer capabilities

Digital Banking

- SC Mobile app for account management, transfers, and bill payments

- Online Banking with full transaction capabilities

- International fund transfer capabilities built into the platform

- Real-time forex rates and conversion

Branch and ATM Network

Standard Chartered operates approximately 10 branches in Sri Lanka, concentrated in Colombo and a few major cities. Their ATM network is similarly limited. You can access the LankaPay network for basic withdrawals, but the physical footprint is the smallest of any bank in this guide.

Honest Assessment: Standard Chartered is a niche product for a niche audience. If you earn Rs. 500,000+ per month, work for a multinational, or plan to relocate overseas, the international connectivity, dedicated relationship manager, and premium service justify the premium threshold. The 360° Rewards programme adds value for frequent spenders, and the preferential forex rates save real money on international transfers.

But for 95% of Sri Lankan salary earners, Standard Chartered is irrelevant. The Rs. 500,000 minimum salary for Priority Banking is 10x the entry threshold at DFCC (Rs. 50,000) and 20x BOC’s entry threshold (Rs. 25,000). The branch network of ~10 locations means you are banking almost entirely digitally. And the rewards programme requires point accumulation and redemption, which is less straightforward than DFCC’s direct cashback. If you do not need international banking, every local bank in this guide offers better value at lower thresholds.

How Do All 12 Salary Accounts Compare?

How Do You Switch Your Salary to a New Bank Account?

Switching your salary account in Sri Lanka takes 2-4 weeks and involves opening the new account, submitting a salary redirect request to your HR department, and updating your standing orders. Most salary accounts open same-day with just your NIC and a salary slip.

Ruwan had been with the same bank for eight years. He assumed switching would be a nightmare involving paperwork, lost direct debits, and weeks without salary access. He was wrong. The entire process took three days.

Here is how to switch your salary savings account in Sri Lanka:

Step 1: Open the new account. Visit the new bank with your NIC, proof of address, and a recent salary slip. Most salary accounts open within the same day. DFCC and several other banks now offer digital onboarding, so you can start the process online.

Step 2: Get the new bank’s details. Note down your new account number, branch code, and bank code. You will need these for the salary redirect.

Step 3: Submit a salary redirect request. Give your HR department or payroll office the new bank details along with a written request to redirect your salary. Most companies process this within one pay cycle.

Step 4: Keep the old account open temporarily. Do not close your old account until at least two salary cycles have landed in the new one. This avoids any gap if payroll processing is delayed.

Step 5: Redirect standing orders and direct debits. Update any loan EMIs (Equated Monthly Installments), insurance premiums, or recurring payments to debit from the new account.

The entire process typically takes 2-4 weeks from start to finish.

Which Salary Account Should You Pick Based on Your Income?